stl

Syntax

stl(data, period, sWindow, [sDegree], [sJump], [tWindow], [tDegree], [tJump],

[lWindow], [lDegree], [lJump], [robust], [inner], [outer])

Details

Use Loess method to decompose a time series into trend, seasonality and randomness. The result is a dictionary with the following keys: trend, seasonal, and residuals. Each key corresponds to a vector with the same length as data.

Parameters

data is a numeric vector.

period is an integer larger than 1 indicating the length of a time-series cycle.

sWindow is either the string "periodic" that means smoothing is effectively replaced by taking the mean, or an odd number no smaller than 7 indicating the span (in lags) of the loess window for seasonal extraction.

sDegree (optional) can be 0, 1 or 2 indicating the degree of locally-fitted polynomial in seasonal extraction. The default value is 1.

sJump (optional) is an integer greater than 1 indicating the number of elements to skip for the smoother in seasonal extraction. The default value is ceil(sWindow/10).

tWindow (optional) is a positive odd number indicating the span (in lags) of the loess window for trend extraction. The default value is the next odd number after 1.5 * period / (1 - (1.5 / sWindow)).

tDegree (optional) can be 0, 1 or 2 indicating the degree of locally-fitted polynomial in trend extraction. The default value is 1.

tJump (optional) is an integer greater than 1 indicating the number of elements to skip for the smoother in trend extraction. The default value is ceil(sWindow/10).

lWindow (optional) is a positive odd number indicating the the span (in lags) of the loess window of the low-pass filter used for each subseries. The default value is the next odd number after period.

lDegree (optional) can be 0, 1 or 2 indicating the degree of locally-fitted polynomial for the subseries low-pass filter. The default value is 1.

lJump (optional) is an integer greater than 1 indicating the number of elements to skip for the smoother in the subseries low-pass filter. The default value is ceil(sWindow/10).

robust (optional) is a Boolean value indicating if robust fitting is used in the loess procedure. The default value is false.

inner (optional) is a positive integer indicating the number of 'inner' (backfitting) iterations; usually very few (2) iterations suffice. If robust=true, the default value of inner is 1; if robust=false, the default value of inner is 2.

outer (optional) is a positive integer indicating the number of 'outer' robustness iterations. If robust=true, the default value of outer is 15; if robust=false, the default value of outer is 0.

Returns

A dictionary with the following keys: trend, seasonal, and residuals. Each key corresponds to a vector with the same length as data.

Examples

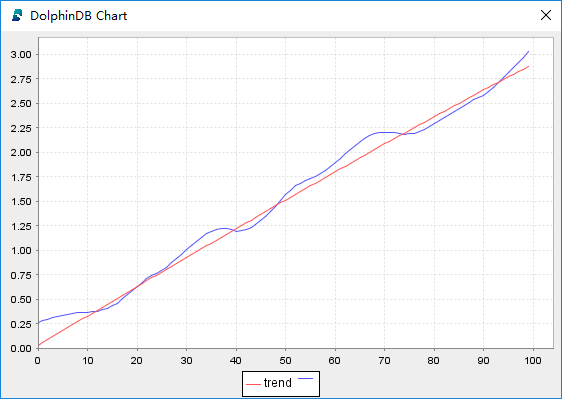

n = 100

trend = 6 * sin(1..n \ 200)

seasonal = sin(pi / 6 * 1..n)

residuals = rand(1.0, n) - 0.5

data = trend + seasonal + residuals

res = stl(data, 12, "periodic");

plot([trend, res.trend]);

plot([seasonal, res.seasonal]);