Applying Low-Frequency Factors to High-Frequency Market Data

In the field of quantitative investment research, factor discovery and application are evolving toward higher-frequency and more granular data. Factor libraries built on DolphinDB, such as 191 Alpha and WorldQuant 101 Alpha, provide a solid foundation for strategy development based on daily and minute-level market data. However, such low-frequency factors are inherently limited in capturing rapidly changing market microstructure dynamics and in extracting more time-sensitive and differentiated trading signals.

As market data becomes increasingly granular, massive volumes of minute-level, snapshot-level, and even tick-by-tick data contain richer information regarding price formation, order flow dynamics, and participant behavior. Robustly extracting alpha signals from high-frequency data and downsampling them for lower-frequency (i.e., daily and hourly) strategy research and portfolio management is now a primary industry focus. Transforming high-frequency data into lower-frequency features enables strategy developers to convert micro-level, transient market states (such as capital flow direction, order book imbalance, and trading impact) into stable, predictive low-frequency features or factors. This facilitates earlier opportunity identification, improved risk management, and the development of differentiated strategies with informational advantages within longer trading horizons.

To address this need, this tutorial presents a professional factor computation solution for minute-level and tick-by-tick financial data, natively built on DolphinDB. The solution leverages DolphinDB’s superior data processing capabilities to adapt over 100 validated mid- to low-frequency factors from public research reports and academic literature to high-frequency data, including minute-level OHLC data, level-2 market snapshots, tick-by-tick orders, and tick-by-tick trades.

1. Introduction to High-Frequency-to-Low-Frequency Factor Library

High-frequency market data refers to data with a time granularity between daily frequency and ultra-high frequency (e.g., millisecond level), primarily including minute-level OHLC data, market snapshots, tick-by-tick trades, and tick-by-tick orders. These datasets record the most granular price movements, order flow dynamics, and trading activities in real time, forming a rich information source for capturing market microstructure and extracting distinctive alpha signals.

Based on established public research reports and academic literature, this tutorial systematically organizes and implements a high-frequency-to-low-frequency factor library. The library covers multiple categories of factors, including price–volume trend factors, volatility factors, and liquidity factors. Its core value lies in providing a fully engineered, performance-optimized, and preliminarily validated standardized factor computation framework. You can directly apply it to high-frequency data to efficiently generate factor series with higher information density, suitable for low-frequency strategy research.

The factor library is natively built on DolphinDB that integrates distributed computing, real-time stream processing, and efficient storage engines. Its multi-paradigm programming language and extensive financial analytics functions are well-suited to handling the substantial throughput and computational complexity of high-frequency data processing, enabling second-level generation of daily factors from terabyte-scale high-frequency datasets. This tutorial provides complete computation scripts and performance benchmarks to facilitate rapid validation, iteration, and deployment of customized low-frequency factors. For the detailed factor list and computation scripts, see Chapter 7.

2. Dataset and Field Specifications

The factor library presented in this tutorial is built on four categories of market data from the Chinese A-share market: minute-level OHLC data, market snapshots, tick-by-tick orders, and tick-by-tick trades. This chapter outlines selected fields and the partitioning schema of the relevant datasets. For the detailed database and table schema design, as well as the code, see Best Practices for Financial Data Storage.

| Dataset | Alias | Partitioned Database Path | Table Name | Partitioning Scheme |

|---|---|---|---|---|

| Minute-level OHLC data | stockMinKSH | dfs://stockMinKSH | stockMinKSH | Partitioned by date |

| Market snapshots | snapshot | dfs://Level2 | snapshot | Partitioned by date + HASH50 by stock symbol |

| Tick-by-tick orders | entrust | dfs://Level2 | entrust | Partitioned by date + HASH50 by stock symbol |

| Tick-by-tick trades | trade | dfs://Level2 | trade | Partitioned by date + HASH50 by stock symbol |

2.1 Minute-Level OHLC Data

Minute-level OHLC data represents the intraday price trajectory at one-minute intervals. It is typically aggregated from tick-by-tick trades and is widely used by short-term traders for intraday price analysis. In this tutorial, the minute-level OHLC data is partitioned by date and stored using the OLAP engine. Each partition contains the minute-level OHLC data for all stocks on the corresponding trading day. The key fields involved in factor computation are listed below:

| Field Name | Data Type | Description |

|---|---|---|

|

SecurityID |

SYMBOL |

Stock symbol |

|

DateTime |

TIMESTAMP |

Trade timestamp |

|

OpenPrice |

DOUBLE |

Open price |

|

HighPrice |

DOUBLE |

High price |

|

LowPrice |

DOUBLE |

Low price |

|

LastPrice |

DOUBLE |

Close price |

|

Volume |

LONG |

Trading volume |

|

Amount |

DOUBLE |

Trading value |

2.2 Level-2 Market Data

Stock level-2 market data includes level-2 snapshots, tick-by-tick orders, and tick-by-tick trades. In a DFS database, join operations across partitioned tables can be time-consuming because the relevant partitions may reside on different nodes, requiring data to be copied between nodes. To address this issue, DolphinDB provides a co-location partitioning mechanism. This allows multiple tables with the same partitioning scheme within a DFS database to store corresponding partitions on the same node, significantly improving join performance. Therefore, in this tutorial, level-2 snapshots, tick-by-tick orders, and tick-by-tick trades—which share the same partitioning scheme—are stored in the same database. The level-2 market data is first partitioned by date and then hash partitioned into 50 partitions by stock symbol, and is stored using the TSDB engine.

2.2.1 Level-2 Market Snapshots

A level-2 market snapshot represents a point-in-time slice of tick-by-tick market data, typically updated every 3 seconds. It includes key information such as multiple levels of bid and ask prices. The key fields involved in factor computation are listed below:

| Field Name | Data Type | Description |

|---|---|---|

|

SecurityID |

SYMBOL |

Stock symbol |

|

TradeTime |

TIMESTAMP |

Data generation timestamp |

|

PreCloPrice |

DOUBLE |

Previous day’s closing price |

|

NumTrades |

INT |

Number of trades |

|

TotalVolumeTrade |

INT |

Total trading volume |

|

TotalValueTrade |

DOUBLE |

Total trading value |

|

LastPrice |

DOUBLE |

Last price |

|

OpenPrice |

DOUBLE |

Open price |

|

HighPrice |

DOUBLE |

High price |

|

LowPrice |

DOUBLE |

Low price |

|

ClosePrice |

DOUBLE |

Today’s close price |

|

TotalBidQty |

INT |

Total bid quantity |

|

TotalOfferQty |

INT |

Total ask quantity |

|

OfferPrice |

DOUBLE VECTOR |

Ask prices (top 10 levels) |

|

BidPrice |

DOUBLE VECTOR |

Bid prices (top 10 levels) |

|

OfferOrderQty |

INT VECTOR |

Ask quantities (top 10 levels) |

|

BidOrderQty |

INT VECTOR |

Bid quantities (top 10 levels) |

|

Market |

SYMBOL |

Exchange name |

2.2.2 Level-2 Tick-by-Tick Orders

Level-2 tick-by-tick orders record every order in the market, including new order submissions, cancellations of existing orders, and modifications to order price or quantity. The key fields involved in factor computation are listed below:

| Field Name | Data Type | Description |

|---|---|---|

|

SecurityID |

SYMBOL |

Stock symbol |

|

TradeTime |

TIMESTAMP |

Quote timestamp |

|

Price |

DOUBLE |

Order price |

|

OrderQty |

INT |

Order quantity |

|

Side |

SYMBOL |

Buy/Sell direction |

|

Market |

SYMBOL |

Exchange name |

2.2.3 Level-2 Tick-by-Tick Trades

Level-2 tick-by-tick trades contain every executed trade reported by the exchange. The data is published every 3 seconds, with each update includes all trades within that interval. Each matched trade consists of a buy order and a sell order, representing the actual transaction process. The key fields involved in factor computation are listed below:

| Field Name | Data Type | Description |

|---|---|---|

|

SecurityID |

SYMBOL |

Stock symbol |

|

TradeTime |

TIMESTAMP |

Trade timestamp |

|

BidApplSeqNum |

LONG |

Buyer order index |

|

OfferApplSeqNum |

LONG |

Seller order index |

|

TradPrice |

DOUBLE |

Trade price |

|

TradeQty |

DOUBLE |

Trade volume |

|

TradeMoney |

DOUBLE |

Trade value |

|

Market |

SYMBOL |

Exchange name |

3. Factor Storage

Factor discovery is a fundamental component of quantitative trading. As the scale of quantitative strategies and AI model training continues to grow, quantitative research teams must handle increasingly large volumes of factor data during the research and development process. Efficient storage of factor data therefore becomes a critical issue. Currently, DolphinDB supports two storage models for factor data: wide tables and narrow tables. Compared with wide tables, narrow tables allow more efficient operations for adding, updating, and deleting factors. Therefore, storing factors using narrow tables is recommended.

3.1 Creating Factor Database

For daily-frequency factor databases, after extensive testing (see Optimal Storage for Trading Factors Calculated at Mid to High Frequencies), the recommended approach is to adopt a composite partitioning scheme of “time dimension by year + factor name.” The data is stored using the TSDB engine, with stock symbol and trade timestamp as the sorting columns. For more recommendations, see Best Practices for Financial Data Storage. The script is shown below:

// Create a database to store daily-frequency factors

create database "dfs://factor_day"

partitioned by RANGE(date(datetimeAdd(1980.01M,0..80*12,'M'))), VALUE(`f1`f2),

engine='TSDB',

atomic='CHUNK'

// Create a partitioned table

create table "dfs://factor_day"."factor_day"(

SecurityID SYMBOL,

TradeDate DATE[comment="time column", compress="delta"],

Value DOUBLE,

FactorName SYMBOL,

UpdateTime TIMESTAMP,

)

partitioned by TradeDate, FactorName

sortColumns=[`SecurityID, `TradeDate],

keepDuplicates=ALL, // Store all written factor values

sortKeyMappingFunction=[hashBucket{, 500}]3.2 Processing Computation Results and Writing to Database

The factor computation result is written to a table with five columns: SecurityID, TradeDate, Value, FactorName, and UpdateTime. Since we recommend storing factors using narrow tables, the computation results can be written directly into the factor database. The corresponding code is as follows:

// Load the table and append the computation results

loadTable("dfs://factor_day","factor_day").append!(select * from res)4. Factor Computation

This chapter describes how to retrieve data, compute factors, and store the results in the database. Some factors have special data requirements or unique computation logic, so their implementation differs from the general factors. These cases will be introduced separately in Section 4.2.

4.1 General Factor Computation

All .dos scripts for factor computation consist of three components:

-

The factor computation functions

-

The background task submission function

-

A factor computation example

You can compute and store factors by configuring the required parameters and executing the script. The following sections describe each component and its usage in detail.

4.1.1 Factor Computation Function

This section defines the factor computation functions. Each function takes the basic data table required for the factor computation as its only input parameter and returns a table in a standardized format. The output table contains five columns: SecurityID, TradeDate, Value, FactorName, and UpdateTime. Each row corresponds to the factor value for a single stock on a specific trading day.

Taking the volume proportion skewness as an example, the corresponding factor computation function is shown below:

def skewVolProp(snapshot){

snap =

select

TradeDate, TradeTime, SecurityID,

deltas(TotalVolumeTrade)\last(TotalVolumeTrade) as volProp

from snapshot

context by TradeDate, SecurityID csort TradeTime

having TradeTime >= 09:30:00.000

// Skewness of the intraday tick-by-tick volume divided by the total volume

res =

select

SecurityID,

TradeDate,

skew(volProp) as Value,

"skewVolProp" as FactorName,

now() as UpdateTime

from snap

group by TradeDate, SecurityID

return res

}4.1.2 Background Task Submission Function

Factor computation typically involves data spanning long periods and can therefore be time-consuming. For this reason, it is more suitable to submit a task to the server for background execution. The function introduced in this section encapsulates the factor computation and storage logic into an executable unit and can run as an asynchronous background task.

The input parameter of the background task submission function is a dictionary containing the basic configuration required for factor computation. The keys are as follows:

| Key | Description | Type |

|---|---|---|

|

func |

Name of the factor computation function |

FUNCTION |

|

funcsec |

Name of the factor adjustment function |

FUNCTION |

|

factorName |

Factor name |

SYMBOL |

|

dataDB |

Database containing the required input data |

STRING |

|

dataTB |

Table containing the required input data |

STRING |

|

factorDB |

Database storing factor results |

STRING |

|

factorTB |

Table storing factor results |

STRING |

|

startDay |

Start date for factor computation |

DATE |

|

endDay |

End date for factor computation |

DATE |

The function first retrieves the partition information of the dataTB table in the dataDB database and generates a ds vector composed of multiple SQL metacode statements. Each SQL statement queries the data within a specified time window for each day between startDay and endDay. These datasets are then used as the data sources for parallel computation tasks.

Next, the function calls the factor computation function in parallel using mr , and merges the computation results from all partitions using unionAll. Finally, the function formats the results according to the schema required by the factorTB table in the factorDB database, and writes the processed data into the target factor database.

Taking the volume proportion skewness as an example, the corresponding background task submission function is shown below:

def factorJob(conf){

dataTB = loadTable(conf[`dataDB], conf[`dataTB])

days = conf[`startDay]..conf[`endDay]

startTime = 09:27:00.000

endTime = 14:57:00.000

//Extract data required for computation and use sqlDS to generate metacode.

ds = sqlDS(<select SecurityID, TradeDate, TradeTime, TotalVolumeTrade

from dataTB

where TradeDate in days and (TradeTime between startTime and endTime) and (SecurityID like "00%" or SecurityID like "30%" or SecurityID like "6%")>)

//The mr function computes the factor in parallel across different nodes, and the unionAll function aggregates the results from all nodes.

res = mr(ds, conf[`func]).unionAll()

//Write the results to the factor database for storage presistence.

loadTable(conf[`factorDB], conf[`factorTB]).append!(select * from res)

}4.1.3 Computation Example

This section provides an example demonstrating parameter configuration and background task submission. First, configure the parameters using the conf dictionary described in Section 4.1.2. Then, submit the task function to the server for background execution using the submitJob function.

Taking the volume proportion skewness as an example, the corresponding computation example is shown below:

// Configure parameters for factor computation.

// conf = {

// func : Name of the factor computation function

// funcsec : Name of the factor adjustment function

// factorName : Factor name

// dataDB : Database containing the required input data

// dataTB : Table containing the required input data

// factorDB : Database storing factor results

// factorTB : Table storing factor results

// startDay : Start date for factor computation

// endDay : End date for factor computation

// }

conf = {

func : skewVolProp,

funcsec : NULL,

factorName : `skewVolProp,

dataDB : "dfs://Level2",

dataTB : "snapshot",

factorDB : "dfs://factor_day",

factorTB : `factor_day,

startDay : 2023.02.01,

endDay : 2023.02.28

}

//Submit a task to the server to compute and store the factor, and return the task ID.

id = submitJob("factor_job", conf[`factorName], factorjob, conf) In this example, the factor name is skewVolProp, and the corresponding

computation function is also skewVolProp . The required

data consists of level-2 market snapshots from February 2023, sourced from

the snapshot table in the dfs://Level2 database. The computation period

ranges from February 1, 2023 to February 28, 2023. The resulting factor

values will be stored in the factor_day table in the dfs://factor_day

database. Since this factor does not require an adjustment function, the

funcsec parameter is set to NULL.

After the configuration is completed, the submitJob

function submits the task to the server for background execution. The

submitted job is named factor_job, with the description skewVolProp, and it

executes the factorJob function described in Section

4.1.2 with conf as the input parameter. Once

submitJob is executed, you only need to wait for the

background task to complete to finish the entire workflow, from factor

computation to database storage.

4.2 Special Factor Computation

Some factors differ from the general factors described above. This section introduces the computation and usage methods for these special cases.

4.2.1 Factors Requiring Additional Datasets

The computation of certain factors involves not only the basic data table but also additional datasets, such as historical data or market index data. In a distributed computing framework, data is processed in parallel across partitions based on time and security identifiers. As a result, some factors—such as those relying on historical windows or external market indices—cannot obtain all required information solely from the currently processed data block.

To address this issue, the factor library allows computation functions to directly read data from databases. For factors requiring additional datasets, the data-loading logic has already been embedded within their computation functions. Therefore, before using these factors, you must modify the database paths for the dependent datasets within the corresponding factor computation functions according to their local environment .

The factors in this library that require additional datasets are listed below:

| Factor Name | Additional Dataset |

|---|---|

|

Daily panic |

Level-2 market snapshots |

|

Intraday active buy proportion |

Level-2 market snapshots |

|

Post-open net active buy proportion |

Level-2 market snapshots |

|

Intraday active buy intensity |

Level-2 market snapshots |

|

Post-open net active buy intensity |

Level-2 market snapshots |

|

Post-open buy intention intensity |

Level-2 tick-by-tick trades |

|

Post-open buy intention proportion |

Level-2 tick-by-tick trades |

Taking the post-open buy intention intensity as an example, the corresponding computation function is shown below:

def netBuyIntenOpen(entrustTB){

//Net increase in buy orders: 1-minute increase in buy orders minus increase in sell orders (tick-by-tick orders)

tmp1 = ...

tmp1 =

select

sum(OrderMoney*iif(Side==`B or Side==`1, 1.0, 0.0)) - sum(OrderMoney*iif(Side==`S or Side==`2, 1.0, 0.0)) as enrustNetBuy

from entrustTB

group by TradeDate, SecurityID, interval(X=TradeTime, duration=60s, label='left', fill=0) as TradeTime

//Net active buy trading value: 1-minute active buy trades minus active sell trades (tick-by-tick trades)

//Query the dependent market data from the tick-by-tick trades table using the instruments from the tick-by-tick orders of the same day

calDate = first(entrustTB[`TradeDate])

codes = exec distinct SecurityID from entrustTB

tradeTB =

select SecurityID, TradeDate, TradeTime, TradePrice*TradeQty as TradeMoney, iif(BidApplSeqNum > OfferApplSeqNum, `B, `S) as BSFlag

from loadTable("dfs://Level2", "trade")

where TradeDate=calDate, SecurityID in codes and TradeTime between 09:30:00.000 and 10:00:00.000, TradePrice>0

tmp2 =

select

sum(TradeMoney*iif(BSFlag==`B, 1.0, 0.0))- sum(TradeMoney*iif(BSFlag==`S, 1.0, 0.0)) as tradeNetBuy,

sum(TradeMoney) as tradeTotal

from tradeTB

group by TradeDate, SecurityID, interval(X=TradeTime, duration=60s, label='left', fill=0) as TradeTime

//Post-open buy intention intensity: mean of the 1-minute buy intention series divided by standard deviation during post-open period (09:30–10:00)

tmp3 =

select

mean(tradeNetBuy+enrustNetBuy)\stdp(tradeNetBuy+enrustNetBuy) as Value

from lj(tmp1, tmp2, `TradeDate`SecurityID`TradeTime)

where tradeNetBuy!=NULL

group by TradeDate, SecurityID

//Factor

res =

select

SecurityID,

TradeDate,

Value,

"netBuyIntenOpen" as FactorName,

now() as UpdateTime

from tmp3

return res

}4.2.2 Re-Adjusted Factors Based on Daily-Frequency Factors

Some factors require secondary adjustments based on generated daily-frequency factors and therefore cannot be computed in a single step. To handle this situation, this section adopts a two-step computation strategy:

-

First, execute the function that computes the daily-frequency factor.

-

Then, pass the resulting output to an adjustment function for further processing.

Because of this workflow, the implementation of these factors differs from the other factors.

From a functional perspective, each factor of this type has two associated functions: one for computing the daily-frequency factors, and another for performing the subsequent adjustment. It should be noted that since the daily-frequency factors have already undergone downsampling, the adjustment step is executed using local computation, which is more efficient than distributed computation.

The main factor of this category included in this factor library is listed below:

| Factor Name | Test Dataset |

|---|---|

|

Adjusted daily ambiguous spread |

Minute-level OHLC data |

Taking the adjusted daily ambiguous spread as an example, the corresponding factor computation function is shown below:

//User-defined factor computation function

def fuzzinessDiff(minKTB){

/**@test Temporary debugging with a small dataset

minKTB =

select SecurityID, date(DateTime) as TradeDate, time(DateTime) as TradeTime, LastPx, Volume, Amount

from loadTable("dfs://stockMinKSH", "stockMinKSH")

where date(DateTime) between 2021.01.04 and 2021.01.31, SecurityID in `603189`000001 and LastPx>0

*/

//Compute fuzziness

fuzziness =

select

SecurityID,

TradeDate,

TradeTime,

Volume,

Amount,

mstd(mstd(percentChange(LastPx), 5, 5), 5, 5) as fuzziness

from minKTB

context by SecurityID, TradeDate

//Compute daily fuzziness threshold and average volume and amount

threshold =

select

SecurityID,

TradeDate,

avg(Volume) as avgVolume,

avg(Amount) as avgAmount,

avg(fuzziness) as thresholdFuzzy

from fuzziness

group by SecurityID, TradeDate

//Daily fuzziness spread = daily fuzziness amount ratio - daily fuzziness volume ratio

res =

select

SecurityID,

TradeDate,

avg(Volume)\first(avgVolume)-avg(Amount)\first(avgAmount) as Value,

"fuzzinessDiff" as factorName,

now() as updateTime

from lj(fuzziness, threshold, `SecurityID`TradeDate)

where fuzziness > thresholdFuzzy

group by SecurityID, TradeDate

return res

}

def adjFuzzinessDiff(diffTB){

/**@test

diffTB = select * from res

*/

//Adjust daily fuzziness spread: sum negative daily fuzziness spreads across the cross-section (s1); divide negative daily fuzziness spreads by their 10-day rolling standard deviation, while positive spreads remain unchanged

s1 =

select

TradeDate,

sum(Value) as s1

from diffTB

where Value<0

group by TradeDate

adjDiff =

select

SecurityID,

TradeDate,

iif(Value<0, Value\mstd(Value, 10), Value) as adjFuzzDiff

from diffTB

context by SecurityID

//Adjust magnitude: sum negative adjusted daily fuzziness spreads across the cross-section (s2); scale negative values by s1/s2

s2 =

s2 =

select

TradeDate,

sum(adjFuzzDiff) as s2

from adjDiff

where adjFuzzDiff<0

group by TradeDate

s =

select

TradeDate,

s1\s2 as s

from ej(s1, s2, `TradeDate)

res =

select

SecurityID,

TradeDate,

iif(adjFuzzDiff<0, adjFuzzDiff*s, adjFuzzDiff) as Value,

"adjFuzzinessDiff" as FactorName,

now() as UpdateTime

from lj(adjDiff, s, `TradeDate)

context by SecurityID, TradeDate

return res

}Since this category of factors requires calling two functions during computation, its task submission function also differs from the general one. The task function for the adjusted ambiguous spread is shown below:

//Sample computation function running in the background

def factorjob(conf){

dataTB = loadTable(conf[`dataDB], conf[`dataTB])

days = conf[`startDay]..conf[`endDay]

startTime = 09:30:00.000

endTime = 14:57:00.000

//Extract data required for computation and use sqlDS to generate metacode.

ds = sqlDS(<select SecurityID, date(DateTime) as TradeDate, time(DateTime) as TradeTime, LastPx, Volume, Amount

from dataTB

where date(DateTime) in days and (time(DateTime) between startTime and endTime) and (SecurityID like "00%" or SecurityID like "30%" or SecurityID like "6%") and LastPx>0>)

//The mr function computes the factor in parallel across different nodes, and the unionAll function aggregates the results from all nodes.

diffTB = mr(ds, conf[`func]).unionAll()

res = conf[`funcsec](diffTB)

//Write the results to the factor database for storage presistence.

loadTable(conf[`factorDB], conf[`factorTB]).append!(select * from res)

} The difference from the general workflow is that this type of computation

requires configuring the funcsec parameter to enable the two-step

process: first, execute the func function in a distributed

manner to generate the daily-freqneucy factors, and then apply the

funcsec function for adjustment. When configuring,

assign the adjustment function to funcsec in conf . An example of

this computation is shown below:

//Sample parameter configuration

conf = {

func : fuzzinessDiff,

funcsec : adjFuzzinessDiff,

factorName : "fuzzinessDiff",

dataDB : "dfs://stockMinKSH",

dataTB : "stockMinKSH",

factorDB : "dfs://factor_day",

factorTB : "factor_day",

startDay : 2021.01.01,

endDay : 2021.01.31

}

//Submit a task to the server to compute and store the factor

id = submitJob("factorjob", conf[`factorname], factorjob, conf)4.3 Batch Factor Computation

This factor library supports batch factor computation. All scripts are ready to use. You only need to configure parameters, upload the scripts to the DolphinDB server, and execute them in a loop to perform batch computation and store the results.

For example, for daily-frequency factors based on tick-by-tick trades, upload

the required scripts to the directory:

/ssd/ssd0/singleDDB/server/HighFrequencyFactorLibrary/DailyFactorsBasedOnTickTrades

.

Then execute the following code to perform batch computation for this category of factors:

//Log on to the server

login("xxxxxx","xxxxxxxx");

go

//Directory for the scripts

scriptdir = "/ssd/ssd0/singleDDB/server/HighFrequencyFactorLibrary/DailyFactorsBasedOnTickTrades"

//Obtain the name of the scripts in the directory

scriptFiles = files(scriptdir)

//Batch run scripts

for(script in scriptFiles){

run(scriptdir+"/"+script[`filename], newSession = true, clean = true)

print("Script executed:"+script[`filename])

}You can configure the script directory and choose whether to print runtime information according to your needs.

4.4 Factor Updates

By default, factors in this library are appended to the end of the target table when written to the database. If you need to update existing factor values, this can be achieved by adjusting the configuration items when creating the factor database. The example below demonstrates the procedure.

//Delete existing databases

if(existsDatabase("dfs://factor_day")) dropDatabase("dfs://factor_day")

//Create database to store daily-frequency factors

create database "dfs://factor_day"

partitioned by RANGE(date(datetimeAdd(1980.01M,0..80*12,'M'))), VALUE(`f1`f2),

engine='TSDB',

atomic='CHUNK'

//Create partitioned table

create table "dfs://factor_day"."factor_day"(

SecurityID SYMBOL,

TradeDate DATE[comment="time column", compress="delta"],

Value DOUBLE,

FactorName SYMBOL,

UpdateTime TIMESTAMP,

)

partitioned by TradeDate, FactorName

sortColumns=[`SecurityID, `TradeDate],

keepDuplicates=LAST, //Support duplicate writing to keep the latest factor values

sortKeyMappingFunction=[hashBucket{, 500}]When creating the table, the keepDuplicates parameter can be set to control the deduplication behavior. Setting it to LAST ensures that, based on the columns specified in sortColumns , only the most recent record for each key is retained in the database. Additionally, the UpdateTime column in the factor table can be used to record the timestampwhen the data was written to the database.

5. Computational Performance

5.1 Test Environment and Datasets

5.1.1 Test Environment

The tests were conducted on DolphinDB server version 2.00.16 with the following hardware configuration:

| Component | Specification |

|---|---|

|

Operating system |

CentOS Linux 7 (Core) |

|

Kernel |

3.10.0-1160.el7.x86_64 |

|

CPU |

Intel(R) Xeon(R) Gold 5220R CPU @ 2.20GHz, 16 logical cores |

|

Memory |

8 × 32GB RDIMM, 3200MT/s, total 256 GB |

|

Disk |

SSD 6 × 3.84TB SATA, read-intensive, 6Gbps, 512 2.5-inch Flex Bay, 1 DWPD Single-disk random write

Single-disk mixed random read/write

|

|

Network |

9.41 Gbps (10 Gigabit Ethernet) |

5.1.2 Test Datasets

The datasets and their volumes used for factor computation are as follows:

| Factor Type | Test Dataset | Number of Records |

|---|---|---|

|

Snapshot-based factors |

Feb 2023 SSE & SZSE level-2 snapshots |

475,627,079 |

|

Tick-by-tick order-based factors |

Feb 2023 SSE & SZS tick-by-tick orders |

2,712,071,019 |

|

Tick-by-tick trade-based factors |

Feb 2023 Shanghai & Shenzhen tick-by-tick trades |

2,067,012,875 |

|

Minute-level OHLC-based factors |

Jan 2021 OHLC data |

38,594,699 |

5.2 Test Results

The computation time for each factor using the test datasets is summarized below:

| Factor Name | Test Dataset | Computation Time (s) |

|---|---|---|

|

Shortest-path illiquidity |

Jan 2021 OHLC data |

0.29 |

|

Consistent buy |

Jan 2021 OHLC data |

0.25 |

|

Absolute return and adjusted lagged volume correlation |

Jan 2021 OHLC data |

78.75 |

|

Volume "tide" price change rate |

Jan 2021 OHLC data |

0.48 |

|

Price drop temporal centroid deviation |

Jan 2021 OHLC data |

77.94 |

|

Consistent trade |

Jan 2021 OHLC data |

0.33 |

|

Turnover proportion entropy |

Jan 2021 OHLC data |

0.23 |

|

Intraday persistent abnormal volume |

Jan 2021 OHLC data |

0.56 |

|

Daily dazzling volatility |

Jan 2021 OHLC data |

0.35 |

|

Daily midday shadow |

Jan 2021 OHLC data |

1.52 |

|

Single turnover proportion entropy |

Jan 2021 OHLC data |

0.27 |

|

Daily post-disaster reconstruction |

Jan 2021 OHLC data |

1.01 |

|

Lagged absolute return and adjusted volume correlation |

Jan 2021 OHLC data |

78.53 |

|

Daily dazzling return |

Jan 2021 OHLC data |

0.27 |

|

Daily peak-climb |

Jan 2021 OHLC data |

1.04 |

|

Absolute return and volume correlation |

Jan 2021 OHLC data |

0.41 |

|

Absolute return and lagged volume correlation |

Jan 2021 OHLC data |

0.18 |

|

Lagged absolute return and volume correlation |

Jan 2021 OHLC data |

0.19 |

|

Daily morning mist |

Jan 2021 OHLC data |

0.92 |

|

T-distribution active proportion |

Jan 2021 OHLC data |

0.61 |

|

Confidence-normal active proportion |

Jan 2021 OHLC data |

0.30 |

|

Naive active proportion |

Jan 2021 OHLC data |

0.63 |

|

T-distribution active proportion |

Jan 2021 OHLC data |

0.21 |

|

Volume peak count |

Jan 2021 OHLC data |

0.22 |

|

Daily ambiguous amount proportion |

Jan 2021 OHLC data |

0.36 |

|

Daily ambiguous number proportion |

Jan 2021 OHLC data |

0.38 |

|

P-type volume distribution |

Jan 2021 OHLC data |

0.42 |

|

B-type volume distribution |

Jan 2021 OHLC data |

0.44 |

|

Adjusted daily ambiguous spread |

Jan 2021 OHLC data |

Base: 0.38; Adjusted: 0.41 |

|

Difference between volume support zone lower bound and closing price |

Jan 2021 OHLC data |

0.43 |

|

Ambiguous correlation |

Jan 2021 OHLC data |

0.32 |

|

Time-weighted relative stock price position |

Feb 2023 Level-2 snapshots |

7.96 |

|

High-frequency upside volatility proportion |

Feb 2023 Level-2 snapshots |

5.94 |

|

High-frequency downside volatility proportion |

Feb 2023 Level-2 snapshots |

5.94 |

|

Realized volatility |

Feb 2023 Level-2 snapshots |

5.78 |

|

Upside realized volatility |

Feb 2023 Level-2 snapshots |

5.20 |

|

Downside realized volatility |

Feb 2023 Level-2 snapshots |

5.05 |

|

High-frequency realized skewness |

Feb 2023 Level-2 snapshots |

5.27 |

|

High-frequency realized kurtosis |

Feb 2023 Level-2 snapshots |

4.93 |

|

Up-down volatility asymmetry |

Feb 2023 Level-2 snapshots |

6.98 |

|

Mid-price change skewness |

Feb 2023 Level-2 snapshots |

30.27 |

|

Mid-price change maximum |

Feb 2023 Level-2 snapshots |

31.44 |

|

Large-volume realized skewness |

Feb 2023 Level-2 snapshots |

7.41 |

|

Large-volume price-volume correlation |

Feb 2023 Level-2 snapshots |

7.35 |

|

Realized bi-power variation |

Feb 2023 Level-2 snapshots |

5.85 |

|

Realized tri-power variation |

Feb 2023 Level-2 snapshots |

6.16 |

|

Daily panic |

Feb 2023 Level-2 snapshots |

4.01 |

|

Volume bucket entropy |

Feb 2023 Level-2 snapshots |

5.68 |

|

Realized jump volatility |

Feb 2023 Level-2 snapshots |

6.72 |

|

Trading volume coefficient of variation |

Feb 2023 Level-2 snapshots |

5.76 |

|

Upside realized jump volatility |

Feb 2023 Level-2 snapshots |

6.34 |

|

Downside realized jump volatility |

Feb 2023 Level-2 snapshots |

6.69 |

|

Smart money |

Feb 2023 Level-2 snapshots |

7.51 |

|

Volume proportion skewness |

Feb 2023 Level-2 snapshots |

5.24 |

|

Volume proportion kurtosis |

Feb 2023 Level-2 snapshots |

5.26 |

|

Daily active trade sentiment |

Feb 2023 Level-2 snapshots |

8.34 |

|

Trend proportion |

Feb 2023 Level-2 snapshots |

6.69 |

|

Up-down jump volatility asymmetry |

Feb 2023 Level-2 snapshots |

6.80 |

|

Maximum price increase |

Feb 2023 Level-2 snapshots |

5.44 |

|

Large-order net inflow rate |

Feb 2023 Level-2 snapshots |

8.35 |

|

Large-order-driven price increase |

Feb 2023 Level-2 snapshots |

7.84 |

|

Local reversal by single trade volume |

Feb 2023 Level-2 snapshots |

8.63 |

|

Average single-trade outflow proportion |

Feb 2023 Level-2 snapshots |

8.03 |

|

Large upside jump volatility |

Feb 2023 Level-2 snapshots |

8.03 |

|

Large downside jump volatility |

Feb 2023 Level-2 snapshots |

8.22 |

|

Small upside jump volatility |

Feb 2023 Level-2 snapshots |

8.13 |

|

Small downside jump volatility |

Feb 2023 Level-2 snapshots |

7.83 |

|

Intraday conditional value-at-risk |

Feb 2023 Level-2 snapshots |

8.73 |

|

Overnight return |

Feb 2023 Level-2 snapshots |

5.18 |

|

Intraday maximum drawdown |

Feb 2023 Level-2 snapshots |

5.09 |

|

Intraday volume proportion standard deviation |

Feb 2023 Level-2 snapshots |

5.26 |

|

Trade-volume return correlation |

Feb 2023 Level-2 snapshots |

8.33 |

|

Intraday return |

Feb 2023 Level-2 snapshots |

5.04 |

|

Minute-level turnover variance |

Feb 2023 Level-2 snapshots |

5.39 |

|

Last half-hour return |

Feb 2023 Level-2 snapshots |

2.03 |

|

Daily order book spread |

Feb 2023 Level-2 snapshots |

30.64 |

|

Last half-hour turnover proportion |

Feb 2023 Level-2 snapshots |

2.04 |

|

Large up-down jump volatility asymmetry |

Feb 2023 Level-2 snapshots |

9.44 |

|

Small up-down jump volatility asymmetry |

Feb 2023 Level-2 snapshots |

10.33 |

|

Daily price elasticity |

Feb 2023 Level-2 snapshots |

7.31 |

|

Daily average order book depth |

Feb 2023 Level-2 snapshots |

29.77 |

|

Weighted close price ratio |

Feb 2023 Level-2 snapshots |

6.32 |

|

Structured reversal |

Feb 2023 Level-2 snapshots |

6.98 |

|

Daily effective depth |

Feb 2023 Level-2 snapshots |

28.92 |

|

Minute-level turnover autocorrelation |

Feb 2023 Level-2 snapshots |

5.60 |

|

Last half-hour turnover proportion |

Feb 2023 Level-2 snapshots |

2.01 |

|

Weighted skewness |

Feb 2023 Level-2 snapshots |

8.94 |

|

Synchronized informed trading probability |

Feb 2023 Level-2 snapshots |

8.52 |

|

Post-open buy intention intensity |

Feb 2023 Level-2 tick-by-tick orders |

11.80 |

|

Post-open net buy order increment propotion |

Feb 2023 Level-2 tick-by-tick orders |

3.56 |

|

Post-open buy intention proportion |

Feb 2023 Level-2 tick-by-tick orders |

5.69 |

|

Selling rebound deviation |

Feb 2023 Level-2 tick-by-tick trades |

87.86 |

|

Large-buy order proportion |

Feb 2023 Level-2 tick-by-tick trades |

38.15 |

|

Buy-order concentration |

Feb 2023 Level-2 tick-by-tick trades |

32.47 |

|

Sell-order concentration |

Feb 2023 Level-2 tick-by-tick trades |

31.79 |

|

Post-open large-order net buy proportion |

Feb 2023 Level-2 tick-by-tick trades |

14.73 |

|

Intraday active buy proportion |

Feb 2023 Level-2 tick-by-tick trades |

49.80 |

|

Large-buy order intensity |

Feb 2023 Level-2 tick-by-tick trades |

38.02 |

|

Post-open net active buy proportion |

Feb 2023 Level-2 tick-by-tick trades |

17.61 |

|

Intraday active buy intensity |

Feb 2023 Level-2 tick-by-tick trades |

38.02 |

|

Post-open net active buy intensity |

Feb 2023 Level-2 tick-by-tick trades |

16.81 |

|

Sell-order illiquidity |

Feb 2023 Level-2 tick-by-tick trades |

29.79 |

|

Buy-order illiquidity |

Feb 2023 Level-2 tick-by-tick trades |

29.64 |

|

Selling rebound proportion |

Feb 2023 Level-2 tick-by-tick trades |

34.94 |

|

Normal large-buy proportion excluding ultra-large orders |

Feb 2023 Level-2 tick-by-tick trades |

35.77 |

|

Ultra-large buy proportion |

Feb 2023 Level-2 tick-by-tick trades |

29.00 |

|

Small-buy order aggressiveness |

Feb 2023 Level-2 tick-by-tick trades |

1,035.52 |

|

Large-order price change excluding ultra-large orders |

Feb 2023 Level-2 tick-by-tick trades |

25.44 |

|

Informed trading probability weighted by physical time |

Feb 2023 Level-2 tick-by-tick trades |

28.24 |

|

Ultra-large order price change |

Feb 2023 Level-2 tick-by-tick trades |

19.43 |

|

Buy floating loss proportion |

Feb 2023 Level-2 tick-by-tick trades |

33.64 |

|

Buy floating loss deviation |

Feb 2023 Level-2 tick-by-tick trades |

20.28 |

|

Post-open large-order net buy intensity |

Feb 2023 Level-2 tick-by-tick trades |

14.06 |

|

Large-volume order turnover proportion |

Feb 2023 Level-2 tick-by-tick trades |

34.27 |

|

Large-volume executed order turnover proportion |

Feb 2023 Level-2 tick-by-tick trades |

31.57 |

6. FAQ

6.1 How do I convert narrow factor tables into a wide format by factor name?

We recommend storing factors in narrow tables. If your require a wide table, you can use DolphinDB’s pivotBy function for conversion. Example:

dailyFactor = loadTable("dfs://factor_day", "factor_day")

factorTB1 = select

Value

from dailyFactor

where FactorName in `skewVolProp`netBuyIntenOpen

pivot by SecurityID, TradeDate, FactorName6.2 How do I convert a wide table back into a narrow table?

You can use DolphinDB’s unpivot function:

factorTB2 =

select

SecurityID, TradeDate, value as Value, valueType as FactorName

from factorTB1.unpivot(`SecurityID`TradeDate, `skewVolProp`netBuyIntenOpen)6.3 How do I store each factor in a separate table?

If you want each factor in its own table within the same database, here’s an example using volume proportion skewness:

// Delete existing databases

if(existsDatabase("dfs://factor_day")) dropDatabase("dfs://factor_day")

// Create database to store daily-frequency databases

create database "dfs://factor_day"

partitioned by RANGE(date(datetimeAdd(1980.01M,0..80*12,'M'))),

engine='TSDB',

atomic='CHUNK'

// Task function

def factorjob(conf){

dataTB = loadTable(conf[`dataDB], conf[`dataTB])

days = conf[`startDay]..conf[`endDay]

startTime = 09:27:00.000

endTime = 14:57:00.000

//Extract data required for computation and use sqlDS to generate metacode.

ds = sqlDS(<select SecurityID, TradeDate, TradeTime, TotalVolumeTrade

from dataTB

where TradeDate in days and (TradeTime between startTime and endTime) and (SecurityID like "00%" or SecurityID like "30%" or SecurityID like "6%")>)

// The mr function computes the factor in parallel across different nodes, and the unionAll function aggregates the results from all nodes.

diffTB = mr(ds, conf[`func]).unionAll()

res = mr(ds, conf[`func]).unionAll()

// Create partitioned table

db = database(conf[`factorDB])

tbName = conf[`factorName]

if(existsTable(conf[`factorDB], tbName)){dropTable(db, tbName)}

colNames = `SecurityID`TradeDate`Value`FactorName`UpdateTime

colTypes = [SYMBOL, DATE, DOUBLE, SYMBOL, TIMESTAMP]

t = table(1000:0, colNames, colTypes)

pt = createPartitionedTable(dbHandle=db,

table=t,

tableName=tbName,

partitionColumns=`TradeDate,

sortColumns=`SecurityID`TradeDate, keepDuplicates=ALL,

sortKeyMappingFunction=[hashBucket{, 500}])

// Write factor to disk

loadTable(conf[`factorDB], conf[`factorName]).append!(select * from res)

}6.4 How do I handle field name mismatch between input data and factor computation?

If your data uses different field names from those listed in this tutorial, the SQL code in the task function that constructs the distributed data source must be adjusted accordingly. For example, for volume proportion skewness, the adjustment might look like this:

def factorjob(conf){

dataTB = loadTable(conf[`dataDB], conf[`dataTB])

days = conf[`startDay]..conf[`endDay]

startTime = 09:27:00.000

endTime = 14:57:00.000

//Extract data required for computation and use sqlDS to generate metacode.

//Modify field names here

ds = sqlDS(<select ticker as SecurityID,

date(tradeTime) as TradeDate,

time(tradeTime) as TradeTime,

cumVolume as TotalVolumeTrade

from dataTB

where date(tradeTime) in days and (time(tradeTime) between startTime and endTime) and (ticker like "00%" or ticker like "30%" or ticker like "6%")>)

//The mr function computes the factor in parallel across different nodes, and the unionAll function aggregates the results from all nodes.

res = mr(ds, conf[`func]).unionAll()

//Write the results to the factor database for storage presistence.

loadTable(conf[`factorDB], conf[`factorTB]).append!(select * from res)

}6.5 How do I perform correlation analysis between factors?

DolphinDB provides multiple built-in functions for correlation analysis, such as corr for computing the Pearson correlation coefficient and spearmanr for computing the Spearman correlation coefficient. This section gives an example of factor correlation analysis. The sample code is as follows:

// Function that computes correlation

def factorCorr(factor1, factor2, method){

con = ej(factor1, factor2, `SecurityID`TradeDate)

if(method == `pearson){

return corr(con[`Value], con[`factor2_Value])

}

if(method == `spearman){

return spearmanr(con[`Value], con[`factor2_Value])

}

if(method == `kendall){

return kendall(con[`Value], con[`factor2_Value])

}

}

// Correlation analysis

factorTB = loadTable("dfs://factor_day", `factor_day)

factor1 = select * from factorTB where FactorName = `skewVolProp

factor2 = select * from factorTB where FactorName = `netBuyIntenOpen

result = factorCorr(factor1, factor2, `pearson)This correlation computation function can compute the Pearson, Spearman, and Kendall correlation coefficients between two factors. The input parameters are two factor tables and the type of correlation coefficient to compute, and the output is a correlation coefficient of type DOUBLE.

7. Factor and Code Summary

7.1 Factor Library Code

All factor scripts in this library are organized in the compressed package. You can extract the package and modify the scripts according to your own database tables.

7.2 List of Factors in Library

7.2.1 Factors Based on Minute-Level OHLC Data

| Factor Name | Computation Logic and Meaning | Reference |

|---|---|---|

|

Shortest-Path illiquidity |

Shortest price movement path :

|

Illiquidity factors constructed based on OHLC paths, Everbright Securities |

|

Consistent buy trading |

Collective consistent trading: OHLC data where

|

Consensus trading factors: capturing returns from collective behavior, Everbright Securities |

|

Absolute return and adjusted lagged volume correlation |

Adjusted volume: Absolute return: absolute value of log return Correlation of absolute return with adjusted lagged volume: correlation between absolute return and adjusted volume at the previous time point |

High-frequency price-volume relations, Founder Securities |

|

Price change rate of volume “tides” |

Domain volume: total volume of the n-th minute and 4 minutes before/after Peak time: moment with maximum domain volume Rising tide time: lowest domain volume before peak at time m Falling tide time: lowest domain volume after peak at time n Tide price change rate: (closing price at rising tide – closing price at falling tide) / (n-m) |

Tidal changes of individual stock volume and “tide” factor construction, Founder Securities |

|

Downside time-center deviation |

Up/down amplitude time center: weighted average time of price movements during up/down periods Downside time-center deviation: residual mean from regressing cross-sectional downside time centers on upside time centers |

Temporal characteristics of intraday minute returns: logical discussion and factor enhancement, Kaiyuan Securities |

|

Consistent trading |

Collective consistent trading: OHLC data

satisfying |

Capturing returns from collective behavior, Everbright Securities |

|

Trading volume propotion entropy |

Entropy of each minute’s trading volume as a fraction of total daily volume |

High-volume trading factor: matching volume and price, Changjiang Securities |

|

Intraday persistent abnormal volume |

Abnormal volume: ratio of current minute’s volume to mean volume over past period (here, past 10 minutes) Persistent abnormal volume:mean(rankATV)/std(rankATV) +

kurt(rankATV), where rankATV

is percentile rank of abnormal volume in the market

cross-section |

“Persistent abnormal trading volume” stock selection factor PATV, China Merchants Securities |

|

Daily dazzling volatility |

Volume surge moments: the times when the increase in trading volume is greater than the daily difference series mean plus 1 standard deviation Dazzling volatility: the 1-minute return standard deviation during the four-minute interval following moments of volume surge Daily dazzling volatility: the mean of all dazzling volatilities within trading day |

Alpha from volume surge moments, Founder Securities |

|

Midday wood |

Ordinary least squares regression with an intercept on the incremental volume data from minute 6 to minute 240 of each trading day:

volDiff is the 1-minute incremental volume. If the F-statistic of the regression is less than its cross-sectional mean, the midday wood factor is set to the negative of the absolute value of the intercept’s t-statistic; otherwise, it is set to the absolute value of the intercept’s t-statistic. |

Decomposition of factors driving stock price changes and “hidden flower in the forest” factor, Founder Securities |

|

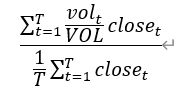

Single volume propotion entropy |

Computed as:

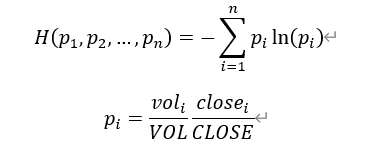

voli and closei are the per-minute trading volume and per-minute closing price, while VOL and CLOSE are the total volume and total closing price over the entire time period. |

High-volume trading factor: matching volume and price, Changjiang Securities |

|

Daily post-disaster reconstruction |

Optimal volatility: the square of the ratio of the standard deviation to the mean of the high-low prices over the current minute and the previous four minutes. Return-volatility ratio: the ratio of the return to the optimal volatility. Daily post-disaster reconstruction: the covariance between the return-volatility ratio and the optimal volatility. |

Constructing volatility changes and “climbing peak” factor, Founder Securities |

|

Lagged absolute return and adjusted volume correlation |

Adjusted turnover: Absolute return: the absolute value of the log return. Lagged absolute return–adjusted turnover correlation: the correlation between the previous minute’s absolute return and the adjusted turnover. |

High-frequency symphony of price-volume relationships, Founder Securities |

|

Daily dazzling return |

Volume surge moments: when the increase in trading volume exceeds the mean of the daily difference series plus one standard deviation. Dazzling return: the one-minute return at times of volume surge. Daily dazzling return: the average of all dazzling returns within a trading day. |

Alpha from volume surge moments, Founder Securities |

|

Daily “climbing peak” |

Optimal volatility ratio: the square of the ratio of the standard deviation to the mean of high-low prices over the current minute and the previous four minutes. Return-volatility ratio: the ratio of the return to the optimal volatility. Periods of abnormally high volatility moments: when the optimal volatility exceeds its intraday mean plus one standard deviation. Daily “climbing peak”: the covariance between the return-volatility ratio series and the optimal volatility series at periods of abnormally high volatility within a trading day. |

Constructing volatility changes and “climbing peak” factor, Founder Securities |

|

Absolute return and volume correlation |

Log return: the logarithm of the ratio of the current price to the price at the previous time point. Absolute return–volume correlation: the correlation between the absolute value of the log return and the trading amount. |

High-frequency symphony of price–volume relationships, Founder Securities |

|

Absolute return and lagged volume correlation |

Absolute return–lagged volume correlation: the correlation between the absolute value of the log return and the trading amount at the previous time point. |

High-frequency symphony of price–volume relationships, Founder Securities |

|

Lagged absolute return and volume correlation |

The correlation between the absolute value of the previous period’s log return and the trading amount. |

High-frequency symphony of price–volume relationships, Founder Securities |

|

Daily morning fog |

Ordinary least squares regression with an intercept on the incremental trading volume data from minute 6 to minute 240 of each trading day:

volDiff denotes the 1-minute incremental trading volume. Daily “morning fog”: the standard deviation of the t-statistics of the regression coefficients from the fifth-order incremental volume regression. |

Decomposition of factors driving stock price changes and “hidden flower in the forest” factor, Founder Securities |

|

T-distribution active proportion |

T-distribution active buy amount :

T-distribution active ratio: the T-distribution active buy amount divided by the total trading amount of the day. |

Active trading proportion under distribution estimation, Changjiang Securities |

|

Confidence normal active proportion |

Confidence normal distribution active buy amount:

Confidence normal distribution active propotion: the confidence normal distribution active buy amount divided by the total trading amount of the day. |

Active trading proportion under distribution estimation, Changjiang Securities |

|

Naive active proportion |

Naive active buy amount:

Naive active propotion: the active buy amount divided by the total trading amount of the day. |

Active trading proportion under distribution estimation, Changjiang Securities |

|

Uniform active proportion |

Naive active buy amount:

Naive active propotion: the naive active buy amount divided by the total trading amount of the day. |

Active trading proportion under distribution estimation, Changjiang Securities |

|

Volume peak count |

Volume peak: a time point when the trading volume is greater than the daily mean volume plus one standard deviation. Volume peak count: counts the number of records where the time difference from the previous record exceeds 1 minute. |

Time-series information in high-frequency volatility, Changjiang Securities |

|

Daily ambiguous amount proportion |

Volatility: standard deviation of returns over the current and previous 4 minutes. Ambiguity: standard deviation of volatility over the current and previous 4 minutes. Foggy moment: a time when ambiguity exceeds the daily mean ambiguity. Foggy amount: average trading amount during foggy moments. Daily ambiguity amount ratio: foggy amount divided by the daily mean trading amount. |

Volatility of volatility and investor ambiguity aversion, Founder Securities |

|

Daily ambiguous count proportion |

Volatility: standard deviation of returns over the current and previous 4 minutes. Ambiguity: standard deviation of volatility over the current and previous 4 minutes. Foggy moment: a time when ambiguity exceeds the daily mean ambiguity. Foggy count: average trading count during foggy moments. Daily ambiguity amount ratio: foggy amount divided by the daily mean trading amount. |

Volatility of volatility and investor ambiguity aversion, Founder Securities |

|

P-shaped volume distribution |

Same-price volume: sum of all trading volumes at the same intraday minute closing price, giving the distribution of volume over price. Volume support point and support area: the price with the highest cumulative volume and its surrounding area (the smallest range where cumulative volume reaches 50% of daily total). P-shaped volume distribution: the difference between the lower bound of the volume support area and the day’s highest price. |

Alpha in volume distribution, Industrial Securities |

|

B-shaped volume distribution |

Same-price volume : sum of all trading volumes at the same intraday minute closing price, giving the distribution of volume over price. Volume support point and support area: the price with the highest cumulative volume and its surrounding area (the smallest range where cumulative volume reaches 50% of daily total). B-shaped volume distribution: the difference between the upper bound of the volume support area and the day’s lowest price. |

Alpha in volume distribution, Industrial Securities |

|

Adjusted daily ambiguous price spread |

Daily ambiguity price spread: daily ambiguous amount ratio minus daily ambiguous count ratio. Adjusted daily ambiguous price spread: sum all negative daily ambiguous price spreads across the cross-section as s1; divide each negative daily ambiguous price spread by the standard deviation of its past 10 days’ daily ambiguous price spreads; keep positive spreads unchanged. Scaled adjustment: sum all negative adjusted daily ambiguous price spreads across the cross-section as s2; scale each negative adjusted spread by dividing by s2 and multiplying by s1. |

Ambiguity about velatlity and investor behaviot, Journal of Financial Economics |

|

Difference between volume support zone lower bound and closing price |

Same-price volume: Sum the trading volumes of minutes with the same closing price during the day to get the distribution of volume across prices. Volume support point and volume support zone: The price with the highest cumulative volume and its surrounding area (the smallest range where cumulative volume reaches 50% of the total daily volume). Difference between volume support zone lower bound and closing price: The difference between the lowest price of the volume support area and the day’s closing price. |

Alpha in volume distribution, Industrial Securities |

|

Ambiguous correlation |

Volatility: The standard deviation of returns over the current and previous 4 minutes. Ambiguity: The standard deviation of volatility over the current and previous 4 minutes. Ambiguous correlation: The correlation coefficient between the ambiguous sequence and the transaction amount sequence at each time point. |

Volatility of volatility and investor ambiguity aversion, Founder Securities |

7.2.2 Factors Based on Level-2 Market Snapshots

| Factor Name | Computation Logic and Meaning | Reference |

|---|---|---|

|

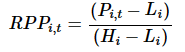

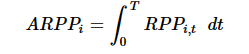

Time-weighted average stock relative price position |

Stock relative price percentile within the high-low range:

Time-weighted average stock relative price position:

|

Measuring intraday buying and selling pressure based on time scale, Orient Securities |

|

High-frequency upside volatility proportion |

Return : price / previous price - 1 Upside return: return > 0 High-frequency upside volatility proportion: sum of squared upward returns / sum of squared returns |

High-frequency factor: decomposition of realized volatility, Guotai Haitong Securities |

|

High-frequency downside volatility proportion |

Return: price / previous price - 1 Downside return: return < 0 High-frequency downside volatility proportion: sum of squared downward returns / sum of squared returns |

High-frequency factor: decomposition of realized volatility, Guotai Haitong Securities |

|

Realized volatility |

Log return series: logarithm of returns Realized volatility: square root of the sum of squared log returns |

The distribution of exchange rate volatlity. Jounal of the Amencan Statistical Association 96,42-55 |

|

Realized upside volatility |

Log return series: logarithm of returns Realized upside volatility: square root of sum of squared positive returns |

Measuting downside risk realised semivariance, In Volatlity and Time Series Econometncs Essays in Honor of Robert F Engle Edited by T Boliersiev.J Russell and M. Watson), Oxford University Press,117-136. |

|

Realized downside volatility |

Log return series: logarithm of returns Realized downside volatility: square root of sum of squared negative returns |

Measuting downside risk realised semivariance, In Volatlity and Time Series Econometncs Essays in Honor of Robert F Engle Edited by T Boliersiev.J Russell and M. Watson), Oxford University Press,117-136. |

|

High-frequency realized skewness |

Return: price / previous price - 1 High-frequency realized skewness: skewness of returns |

High-frequency factor: stock return distribution characteristics, Guotai Haitong Securities |

|

High-frequency realized kurtosis |

Return: price / previous price - 1 High-frequency realized kurtosis: kurtosis of returns |

High-frequency factor: stock return distribution characteristics, Guotai Haitong Securities |

|

Upside-downside volatility asymmetry |

Realized volatility: sum of squared log returns Upside realized volatility: sum of squared positive returns Downside realized volatility: sum of squared negative returns Asymmetry: (Upside realized volatility - Downside realized volatility) / Realized volatility |

Measuting downside risk realised semivariance, In Volatlity and Time Series Econometncs Essays in Honor of Robert F Engle Edited by T Boliersiev.J Russell and M. Watson), Oxford University Press,117-136. |

|

Mid-price change rate skewness |

Market mid-price: average of best bid and ask Mid-price change rate: (current mid-price / previous mid-price) - 1 Skewness of mid-price change rate |

High-frequency order imbalance and spread factors, China Securities |

|

Mid-price change rate maximum |

Market mid-price: average of best bid and ask Mid-price change rate: (current mid-price / previous mid-price) - 1 Maximum mid-price change rate |

High-frequency order imbalance and spread factors, China Securities |

|

Large volume realized skewness |

Large volume: minute volume in the top 1/3 of the day Realized skewness for large volumes: skewness of returns for large-volume orders |

Factorization method for high-frequency price-volume data, GF Securities |

|

Large volume price-volume correlation |

Large volume: minute volume in the top 1/3 of the day Correlation between price and volume for large-volume orders |

Factorization method for high-frequency price-volume data, GF Securities |

|

Realized bipower variation |

Realized bipower variation: sum of products of absolute log returns and previous absolute log returns |

Power and bipower variation with stochastic volatility and jumps. Journal of Financial Econometrics.2.1-48 |

|

Realized tripower variation |

Tripower variation: computes the 2/3 power of products of absolute log returns at t, t-1, and t-2, then sum over the day |

Power and bipower variation with stochastic volatility and jumps. Journal of Financial Econometrics.2.1-48 |

|

Daily panic |

Deviation: absolute difference between the stock return and the market return (using CSI All Share Index 000985 to represent the market). Benchmark term: sum of the absolute value of the stock return, the absolute value of the market return, and 0.1. Daily panic: ratio of deviation to the benchmark term. |

Significant effect, extreme return distortion decision weight, and “All is Alarm” Factor, 2022, Founder Securities. Cosemans M, Frehen R.2021, Salience theory and stock prices: Empirical evidence, Journal of Financial Economics.140(2),480-483 |

|

Volume bucket entropy |

Divide intraday minute-level volumes into equal-width buckets based on max-min range; compute probability for each bucket Entropy: sum of pk * ln(pk) for all buckets, multiplied by -1 |

Alpha in volume distribution, Industrial Securities |

|

Realized jump volatility |

Realized tripower variation: First, compute the 2/3 power of the product of absolute log returns at each time with those at t‑1 and t‑2; then sum all these values within the trading day. Integrated volatility estimator: Realized tripower variation multiplied by the constant 1.935792405 (the 2/3‑order absolute moment of the normal distribution). Realized jump volatility: max(sum of squared log returns minus the integrated volatility estimator, 0). |

Power and bipower variation with stochastic volatility and jumps. Journal of Financial Econometrics.2.1-48. New Evidence of the Marginal Predictve Content of Small and Large Jumps in the Cross-Section, Econometrics, MDPI, 8(2), 1-52. |

|

Volume coefficient of variation |

The standard deviation of the intraday trading volume series divided by its mean. |

Tracking informed traders, China Merchants Securities |

|

Upside realized jump volatility |

Realized tripower variation: First, for each time point, compute the product of the absolute values of log returns at t, t-1, and t-2 raised to the 2/3 power; then sum all these values over the trading day. Integrated volatility estimator: Realized tripower variation multiplied by the constant 1.935792405 (the 2/3-order absolute moment of the normal distribution). Upside realized jump volatility: max(sum of squared log returns where returns > 0 minus half of the integrated volatility estimator, 0). |

New Evidence of the Marginal Predictve Content of Small and Large Jumps in the Cross-Section, Econometrics, MDPI, 8(2), 1-52. |

|

Downside realized jump volatility |

Realized tripower variation: First, for each time point, compute the product of the absolute values of log returns at t, t-1, and t-2, raised to the 2/3 power; then sum all these values over the trading day. Integrated volatility estimator: Realized tripower variation multiplied by the constant 1.935792405 (the 2/3-order absolute moment of the normal distribution). Downside realized jump volatility: max(sum of squared log returns where returns < 0 minus half of the integrated volatility estimator, 0) |

New Evidence of the Marginal Predictve Content of Small and Large Jumps in the Cross-Section, Econometrics, MDPI, 8(2), 1-52. |

|

Smart money |

Raw smart money: the ratio of the absolute value of each minute’s return to the fourth root of its trading volume. Smart money trades: select the minutes with the highest raw smart money factor until their cumulative trading volume reaches 20% of the day’s total. Volume-weighted average price (VWAP): compute the price weighted by trading volume. Smart money: the VWAP of smart money trades divided by the VWAP of all trades. |

Smart money factor model v2.0, Kaiyuan Securities |

|

Volume proportion skewness |

Skewness of intraday volume proportion series |

High-frequency factors IV: higher-moment factors, Changjiang Securities |

|

Volume proportion kurtosis |

Kurtosis of intraday volume proportion series |

High-frequency factors IV: higher-moment factors, Changjiang Securities |

|

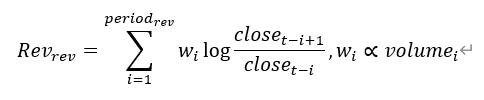

Daily main force trading sentiment |

Rank correlation between individual transaction amount series and close price series |

High-frequency factor: characterization of main force behavior in minute-level trades, Kaiyuan Securities |

|

Trend proportion |

(Daily close - daily open) / sum of absolute price changes at each moment |

Factorization method for high-frequency price-volume data, GF Securities |

|

Upside-downside jump volatility asymmetry |

Realized tripower variation: first, compute the product of the absolute values of log returns at times t, t‑1, and t‑2, raised to the 2/3 power for each minute; then sum all these values within the trading day. Integrated volatility estimate: realized tripower variation multiplied by the constant 1.935792405 (the 2/3‑order absolute moment of a normal distribution). Upside (downside) realized jump volatility : max(sum of squared log returns >0 (<0) minus half of the integrated volatility estimate, 0). Asymmetry of upside/downside jump volatility : difference between the upside and downside realized jump volatilities. |

New Evidence of the Marginal Predictve Content of Small and Large Jumps in the Cross-Section, Econometrics, MDPI, 8(2), 1-52. |

|

Maximum intraday return |

Product of (1 + return) over the top 10% intraday returns |

High-frequency stock selection factor taxonomy, CSC Securities |

|

Large trade net inflow rate |

Average trade amount per minute: total amount / number of trades Large trade filter: top 30% average trade amount Net inflow: sum of positive-return trades - sum of negative-return trades Net inflow rate: net inflow / total daily volume |

Intraday trades insights, Guotai Haitong Securities |

|

Large order-driven return |

Average trade amount: total transaction amount per minute divided by the number of trades. Large trade filter: time points where the average trade amount ranks in the top 30%. Large-trade driven return: cumulative product of (large-trade returns + 1). |

Intraday trades insights, Guotai Haitong Securities |

|

Local reversal by trade |

Sum of returns during periods where trade size (volume / number of trades) is in the 80–100% percentile |

Micro-level reversal outcomes in price-volume relationships, Changjiang Securities |

|

Average trade outflow proportion |

Average trade amount with negative return / overall average trade amount |

Intraday trades insights, Guotai Haitong Securities |

|

Large upside jump volatility |

Upside realized jump volatility: max(difference between the sum of squared log returns where returns are greater than 0 and half of the integrated volatility estimator, 0) Discrimination threshold:

where α is an empirical parameter equal to 4, Δ is the intraday sampling interval of stock returns, and IV is the integrated volatility estimator. Large upside jump volatility: min(upside realized jump volatility, sum of squared log returns that exceed the discrimination threshold) |

Empincal evidence on the importance of aggregaton, asymmetry and jumps for volatlty ored cnon jourral af Econometrics.187 606-621 New Evidence of the Marginal Predictve Content of Small and Large Jumps in the Cross-Section, Econometrics, MDPI, 8(2), 1-52. |

|

Large downside jump volatility |

Downside realized jump volatility: max(difference between the sum of squared log returns where returns are less than 0 and half of the integrated volatility estimator, 0) Discrimination threshold:

where α is an empirical parameter equal to 4, Δ is the intraday sampling interval of stock returns, and IV is the integrated volatility estimator. Large downside jump volatility: min(downside realized jump volatility, the sum of squared log returns that are lower than the negative of the discrimination threshold) |

Empincal evidence on the importance of aggregaton, asymmetry and jumps for volatlty ored cnon jourral af Econometrics.187 606-621 New Evidence of the Marginal Predictve Content of Small and Large Jumps in the Cross-Section, Econometrics, MDPI, 8(2), 1-52. |

|

Small upside jump volatility |

Upside realized jump volatility: max(difference between the sum of squared log returns where returns are greater than 0 and half of the integrated volatility estimator, 0) Discrimination threshold:

where α is an empirical parameter equal to 4, Δ is the intraday sampling interval of stock returns, and IV is the integrated volatility estimator. Large upside jump volatility: min(upside realized jump volatility, sum of squared log returns that exceed the discrimination threshold) Small upside jump volatility: difference between the upside realized jump volatility and the large upside jump volatility. |

Empincal evidence on the importance of aggregaton, asymmetry and jumps for volatlty ored cnon jourral af Econometrics.187 606-621 New Evidence of the Marginal Predictve Content of Small and Large Jumps in the Cross-Section, Econometrics, MDPI, 8(2), 1-52. |

|

Small downside jump volatility |

Downside realized jump volatility: max(difference between the sum of squared log returns where returns are less than 0 and half of the integrated volatility estimator, 0) Discrimination threshold:

where, α is an empirical parameter equal to 4, Δ is the intraday sampling interval of stock returns, and IV is the integrated volatility estimator. Large downside jump volatility: min(downside realized jump volatility, sum of squared log returns that are lower than the negative of the discrimination threshold) Small downside jump volatility: difference between the downside realized jump volatility and the large downside jump volatility. |

Empincal evidence on the importance of aggregaton, asymmetry and jumps for volatlty ored cnon jourral af Econometrics.187 606-621 New Evidence of the Marginal Predictve Content of Small and Large Jumps in the Cross-Section, Econometrics, MDPI, 8(2), 1-52. |

|

Intraday conditional value-at-risk |

Minute VWAR: the volume-weighted average of the minute return series. VaR:

CVaR:

VCVaR: CVaR of the intraday minute VWAR at confidence level α. |

Tail characteristics of minute-level data, Founder Securities |

|

Overnight return |

Ratio of the current day’s opening price to the previous day’s closing price minus 1. |