Real-Time Implied Volatility Calculation and Curve Construction for Commodity Options

In the futures and options market, implied volatility (IV) plays a critical role as it helps investors and traders better understand and manage risk, while providing an important reference for decision-making. High volatility usually indicates larger price fluctuations and higher risk. In such conditions, traders may reduce position sizes to limit potential losses. Conversely, during periods of low volatility, they may increase exposure in pursuit of higher returns. By calculating and monitoring volatility, traders can choose appropriate strategies, implement suitable risk controls, and anticipate future market movements. At the same time, the Greeks quantify the sensitivity of option prices to changes in market factors, enabling traders to hedge risk effectively and optimize quoting strategies.

However, option market prices and returns contain substantial noise and fluctuation, which may make the calculated volatility highly variable. Moreover, market volatility is usually not constant; it changes over time and with market conditions, and return distributions are often skewed. Volatility fitting helps improve the accuracy of volatility estimates and allows the volatility curve to better capture the market's complexity and nonlinear characteristics.

Based on DolphinDB's streaming processing framework, this tutorial performs real-time calculation of IV and Greeks for commodity options, and fits volatility curves every minute.

Note: All code in this tutorial is compatible with DolphinDB 2.00.13, 3.00.3, and later versions.

1. Scenario Overview

In the futures and options market, real-time IV is typically calculated based on the Black-Scholes (BS) model. The BS model assumes that the underlying price follows a lognormal distribution and derives the theoretical price of a European option from the no-arbitrage pricing principle. Its core formula values an option using five variables: the underlying price, strike price, time to maturity, risk-free interest rate, and volatility. However, the BS model assumes that the underlying asset is infinitely divisible and pays no dividends, which limits its applicability to futures and options. Its variant, the Black-76 model, replaces the underlying price with the futures price and adjusts the pricing logic based on the relationship between the futures and option maturities. This makes it more suitable for commodity futures options and interest rate futures options. In particular, it provides improved accuracy when the underlying involves storage costs or convenience yields. The formulas are as follows:

Where:

-

F: current price of the underlying futures contract

-

K: option strike price

-

T: time to maturity, in years

-

r: risk-free interest rate with continuous compounding

-

σ: annualized volatility of the futures price

-

N(…): cumulative distribution function of the standard normal distribution

This tutorial calculates IV based on the Black-76 model. Common algorithms for calculating IV under the Black-76 model include the Newton-Raphson method, the bisection method, and Brent's method. Compared with the other two algorithms, Brent's method combines bisection with inverse quadratic interpolation in a hybrid optimization algorithm that offers both stability and fast convergence. DolphinDB also provides a dedicated function for this method; see brentq for details. For implementations and applications of other algorithms, see the tutorial Calculating ETF Option Implied Volatility and Greeks.

2. Implementation Approach

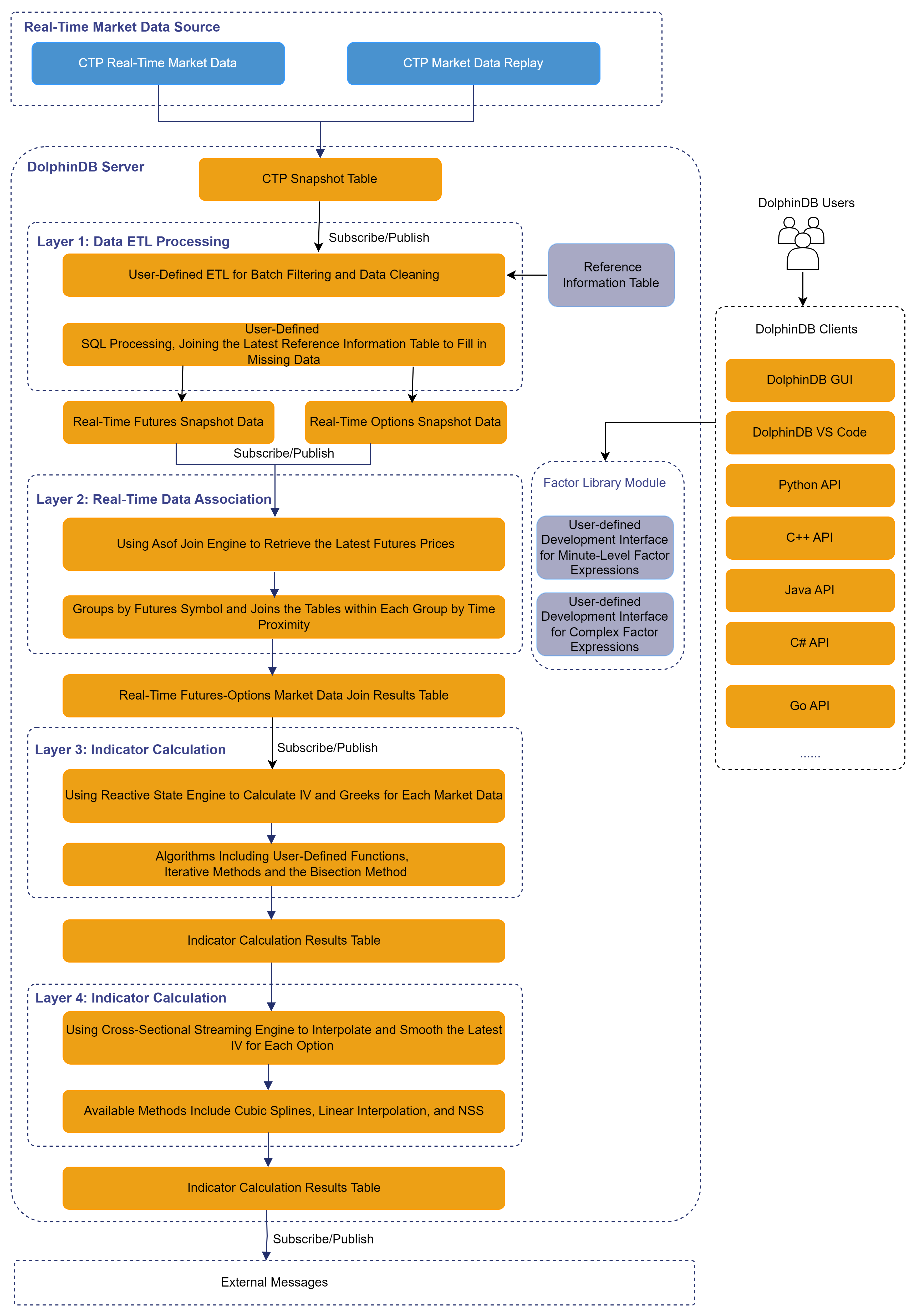

This section explains how DolphinDB uses the streaming engine to implement real-time IV calculation, Greeks calculation, volatility smile construction, and smoothing. The implementation architecture is shown below:

For live trading environments, DolphinDB provides a CTP plugin to ingest tick market data.

For research environments, DolphinDB provides the replay function to

replay historical data and simulate real-time market data: Historical Data

Replay.

After market data is ingested, the workflow mainly consists of the following steps:

-

Data validation and filtering: In this tutorial, real-time market data undergoes a basic filtering process, including conditions such as: bid/ask prices and trading volume must be greater than zero; timestamps must fall within trading hours; and the time difference between data arrival and the actual trade timestamp must not exceed 5 seconds. You can add more filtering rules as needed. During filtering, we also use the reference information table to fill in required fields. After filtering, futures market data and options market data are stored in separate stream tables.

-

Futures price selection: To calculate option IV, an appropriate futures price must be determined. In this tutorial, the futures price is selected as the nearest available observation in time relative to each option quote timestamp. This is implemented using DolphinDB’s Asof Join Engine, which performs time-nearest matching between futures and options streams. The resulting dataset combines option prices, the most recent futures prices, and relevant reference information into a single stream table.

-

IV and Greeks calculation: As described in previous sections, the model and algorithm methods have already been introduced. Here, a Reactive State Engine is used to calculate IV and Greeks independently for each valid market data record.

-

Volatility smile construction and smoothing:

-

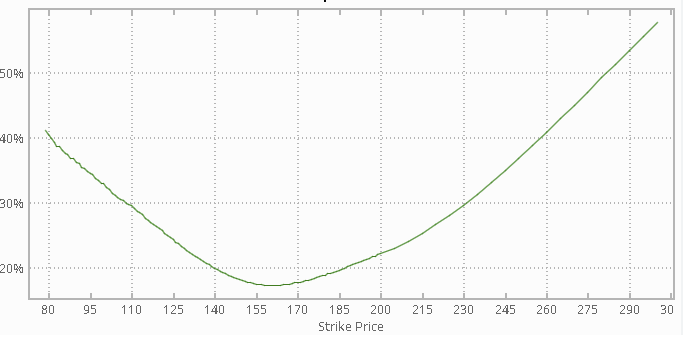

IV curves are generally constructed from more liquid out-of-the-money (OTM) options. In this example, a real-time volatility curve is constructed every minute. Since some contracts have low trading frequency and may not generate continuous updates, a Cross-Sectional Engine is used instead of a Time-Series Engine. At each timestamp, the latest IV for each strike price is used to construct the curve.

-

Curve smoothing: Due to missing observations, market noise, and volatility fluctuations, the resulting volatility curve may appear irregular. To address this, cubic spline interpolation is applied for smoothing. DolphinDB provides a built-in function cubicSpline for this purpose. In addition, functions such as linearInterpolateFit, pchipInterpolateFit, and nss are also available, allowing users to choose the most appropriate method for curve fitting and smoothing according to their needs.

-

3. Data Description

The futures options market data used in this tutorial comes from real-time CTP data. CTP, short for Comprehensive Transaction Platform, is a business management system for the futures market. DolphinDB provides a CTP plugin that connects to the CTP system to subscribe to real-time market data from the futures market and query instrument information. The schema of the CTP real-time market data table is as follows:

| Field name | Data type | Description |

|---|---|---|

| TradingDay | DATE | Trade date |

| ...... | ...... | ...... |

| UpdateTime | SECOND | Trade time, in seconds |

| UpdateMillisec | INT | Trade time, in milliseconds |

| BidPrice1 | DOUBLE | Bid price |

| BidVolume1 | INT | Bid volume |

| AskPrice1 | DOUBLE | Ask price |

| ...... | ...... | ...... |

| InstrumentID | STRING | Option or futures symbol |

| ...... | ...... | ...... |

In addition to the raw market data, this tutorial also uses futures and options reference data from the CTP system, which is further processed for downstream calculations. The table schema is as follows:

| Field name | Data type | Description |

|---|---|---|

| ExchangeID | SYMBOL | Exchange code |

| InstrumentName | STRING | Contract name |

| ....... | ...... | ...... |

| CreateDate | DATE | Creation date |

| OpenDate | DATE | Listing date |

| ExpireDate | DATE | Expiration date |

| ...... | ....... | ...... |

| StrikePrice | DOUBLE | Strike price |

| OptionsType | SYMBOL | Option type |

| UnderlyingMultiple | DOUBLE | Underlying multiplier |

| CombinationType | SYMBOL | Combination type |

| InstrumentID | SYMBOL | Contract code |

| ExchangeInstID | SYMBOL | Exchange instrument ID |

| ProductID | SYMBOL | Product code |

| UnderlyingInstrID | SYMBOL | Underlying instrument code |

| insertTime | TIMESTAMP | Update time |

| prdCode | SYMBOL | Instrument symbol |

4. Implementation

The appendix at the end of this tutorial provides sample data, as well as scripts to create the database and tables, and to import the data. After executing the database and table creation scripts, the following script can be used to import the test data:

YourDir = ""

// Import reference data

schemaInfo = select name,typeString from loadTable("dfs://option_info", "data").schema().colDefs

t = loadText(filename=YourDir+"option_info.csv", schema=schemaInfo)

tableInsert(loadTable("dfs://option_info", "data"), t)

// Import futures and options market data

schemaMarket = select name,typeString from loadTable("dfs://ctp", "market").schema().colDefs

loadTextEx(dbHandle=database("dfs://ctp"), tableName="market", partitionColumns=["TradingDay","InstrumentID"], filename=YourDir+"market.csv", schema=schemaMarket)Once the import is completed successfully, execute the appendix scripts in the following order: environment_initialization.dos, function_engine_definitions.dos, and data_replay.dos. You can then quickly experience real-time IV calculation and curve construction.

4.1 Futures Price Selection

As mentioned earlier, DolphinDB provides an asof join engine for time-nearest matching between left and right tables. This makes it straightforward to retrieve the nearest futures price based on the option quote timestamp, as shown below:

ajEngine = createAsofJoinEngine(

name="asofJoin",

leftTable=ctpOptions,

rightTable=ctpFutures,

outputTable=futOptCrt,

metrics=<[ctpOptions.InstrumentID, ctpFutures.assetCode, (ctpFutures.BidPrice1+ctpFutures.AskPrice1)\2, (ctpOptions.BidPrice1+ctpOptions.AskPrice1)\2, KPrice, CPMode, endDate]>,

matchingColumn=[[`futureCode],[`InstrumentID]],

timeColumn=`TradingTime,

useSystemTime=false)

// subscription topic

subscribeTable(tableName="ctpOptions", actionName="appendLeftStream", handler=getLeftStream(ajEngine), msgAsTable=true, offset=-1, hash=0)

subscribeTable(tableName="ctpFutures", actionName="appendRightStream", handler=getRightStream(ajEngine), msgAsTable=true, offset=-1, hash=1)Here, option market data is in the left table, and futures market data is in the right table. For each option quote, the engine retrieves the most recent futures quote and outputs the joined result. You can use the delayedTime parameter to configure the timeout-based forced trigger rule. For details, see the Asof Join Engine documentation.

4.2 IV Calculation

The brent function requires a function argument f and

finds a root x0 of f(x) over a given interval [a,b] such that f(x0)=0.

Therefore, in addition to implementing the Black-76 model, the code also defines

a function loss_function that returns the difference between

theoretical and market prices, and then solves it with the

brent function. The calculation code is as follows:

/** @Brief: Calculates IV using the Black-76 formula

* @Param: F: Current price of the underlying futures contract

* @Param: K: Strike price

* @Param: T: Time to maturity

* @Param: r: Risk-free interest rate

* @Param: sigma: Volatility

* @Param: option_type: Option type, 1 or -1, representing 'C' or 'P'*/

def black_76(F, K, T, r, sigma, option_type){

d1 = (log(F \ K) + (0.5 * pow(sigma , 2) ) * T) \ (sigma * sqrt(T))

d2 = d1 - sigma * sqrt(T)

if (option_type == 1){

return exp(-r * T) * (F * cdfNormal(0,1,d1) - K * cdfNormal(0,1,d2))

}else if( option_type == -1){

return exp(-r * T) * (K * cdfNormal(0,1,-d2) - F * cdfNormal(0,1,-d1))

}else{

return ("Option type must be 1 or -1.")

}

}

/** @Brief: Solver function for IV using Brentq

* @Param: sigma: Volatility

* @Param: F: Current price of the underlying futures contract

* @Param: K: Strike price

* @Param: T: Time to maturity

* @Param: r: Risk-free interest rate

* @Param: option_type: Option type, 1 or -1, representing 'C' or 'P'

* @Param: market_price: Option price*/

def loss_function(sigma, F, K, T, r, option_type, market_price){

return black_76(F, K, T, r, sigma, option_type) - market_price

}

/*** @Brief: Calculates IV using Brentq

* @Param: F: Current price of the underlying futures contract

* @Param: K: Strike price

* @Param: T: Time to maturity

* @Param: r: Risk-free interest rate

* @Param: option_type: Option type, 1 or -1, representing 'C' or 'P'

* @Param: market_price: Option price

* @Return:

* @Sample usage:*/

def implied_volatility_Black76Brentq(F, K, T, r, option_type, market_price){

iv = double(NULL)

try{

iv = brentq(f=loss_function, a=1e-6, b=2, xtol=2e-12, rtol=1e-9, maxIter=100, funcDataParam=[F, K, T, r, option_type, market_price])[1]

}catch(ex){

writeLog("calculate error: " + ex)

}

return iv

}4.3 Volatility Curve Construction and Smoothing

DolphinDB's cross-sectional engine retains the latest record for each group, effectively addressing missing market data for some contracts due to infrequent trading. In addition, the cross-sectional engine can be triggered at fixed intervals based on event time. Here, a cross-sectional engine is created to construct and smooth volatility curves every minute of event time. The code is as follows:

crossEngine = createCrossSectionalEngine(

name="crossEngine",

metrics=<[last(assetCode), buildIVCurve(trigger, futureCode, assetCode, futurePrice, KPrice, CPMode, iv)]>,

dummyTable=ivResult,

outputTable=ivCurve,

keyColumn=`futureCode`KPrice`CPMode,

triggeringPattern='dataInterval',

triggeringInterval=60*1000,

timeColumn=`trigger,

useSystemTime=false,

contextByColumn=`futureCode,

outputElapsedMicroseconds=true)

filterFn = def (msg) { // Filter out records with invalid IV

return (select * from msg where iv > 0)

}

subscribeTable(tableName="ivResult", actionName="buildCurve", offset=-1, handler=append!{crossEngine}, msgAsTable=true, batchSize=10000, throttle=1, hash=3, filter=filterFn);In practice, volatility curves are typically constructed using more liquid OTM options. The latest futures price for each minute is used as the benchmark to identify OTM call and put options. The code is as follows:

strikePrices = KPrice[KPrice< lastPrice and CPMode == -1].join(KPrice[KPrice>= lastPrice and CPMode == 1])

strikeIvs = iv[KPrice< lastPrice and CPMode == -1].join(iv[KPrice>= lastPrice and CPMode == 1])

indexes = isort(strikePrices) // Sort

strikePrices = strikePrices[indexes]

strikeIvs = strikeIvs[indexes]This tutorial applies cubic spline interpolation for curve smoothing. First, a spline model is constructed using the selected OTM options and their implied volatilities. The strike price range is then evenly divided into 50 segments, and the fitted model is used to interpolate implied volatilities at the generated strike prices. Finally, it stores the original strike prices and implied volatilities together with the smoothed strike prices and interpolated implied volatilities in array vectors. The code is as follows:

n = 50 // Sample count

if(strikePrices.size() >= 3 ){ // Do not fit the curve if there are too few volatility data points

// Construct the strike price coordinates for the smile curve

curvePrices = linspace(min(strikePrices), max(strikePrices), n, true)[1]$int

// Construct the cubic spline interpolation model

cs = cubicSpline(strikePrices, strikeIvs)

// Interpolate to obtain the volatility data for the smile curve

curveIvs = cubicSplinePredict(cs, curvePrices)

// Return the interpolation results

tableInsert(objByName(`interResult), ( max(trigger), first(futureCode), first(assetCode), arrayVector([strikePrices.size()], strikePrices), arrayVector([strikeIvs.size()], strikeIvs), arrayVector([curvePrices.size()], curvePrices), arrayVector([curveIvs.size()], curveIvs) ))

}else{

prices, ivs = NULL, NULL

if(strikePrices.count()>0) prices, ivs = arrayVector([strikePrices.size()], strikePrices), arrayVector([strikeIvs.size()], strikeIvs)

tableInsert(objByName(`interResult), ( max(trigger), first(futureCode), first(assetCode), prices, ivs, NULL, NULL ))

}5. Results Visualization

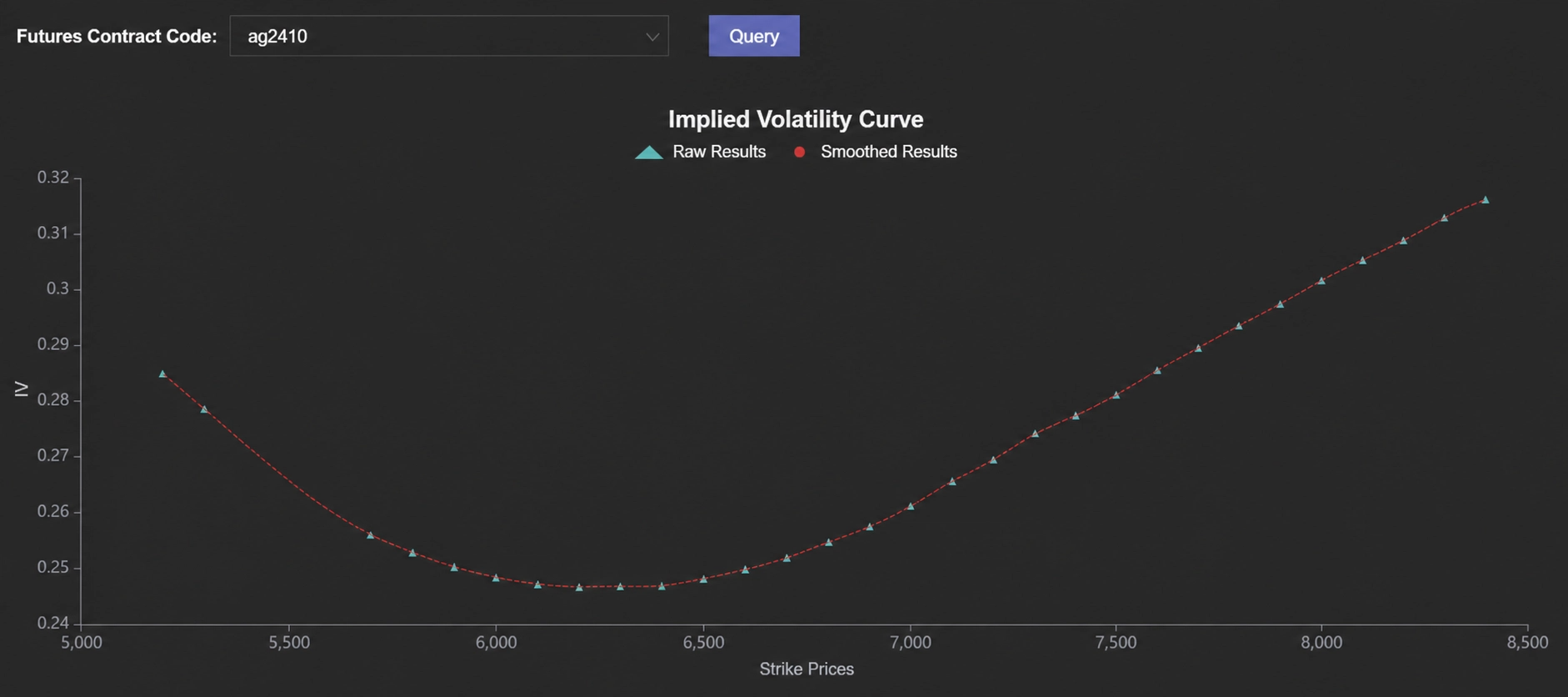

DolphinDB provides a visualization Dashboard that enables real-time volatility curve construction with scheduled refresh. The resulting visualization is shown below:

6. Summary

Based on DolphinDB's streaming processing framework, this tutorial systematically introduces the real-time calculation of IV and Greeks for commodity options, as well as volatility curve construction, fitting and smoothing. It demonstrates how to leverage DolphinDB streaming engines, combined with the Black–76 model and the Brent’s method, to calculate IV and option Greeks in real time. By utilizing mechanisms such as asof joins and cross-sectional engines, the system achieves futures price selection, real-time market data filtering, and dynamic volatility curve construction, followed by cubic spline interpolation for smoothing. Finally, real-time volatility curves are visualized through the DolphinDB Dashboard.

7. Appendices

Database and table creation scripts: database_table_creation.dos

Tutorial dataset: data.zip

Data import script: csv_import.dos

Environment initialization script: 1.environment_initialization.dos

Streaming engine and function definitions: 2.function_engine_definitions.dos

Data replay script: 3.data_replay.dos

Dashboard display template: dashboard.json