Backtesting Application: Medium- and High-Frequency Options Spread Strategy with Volatility Timing

In today’s highly sophisticated derivatives markets, options and their combination strategies have become essential tools for institutional investors to conduct refined risk management and generate alpha. Implied volatility (IV), a core parameter in option pricing, often exhibits short-term fluctuations that create abundant trading opportunities. By constructing multi-leg option portfolios, traders can capture volatility-driven returns while limiting directional exposure.

Before deploying complex strategies involving multi-leg structures, high-frequency signal generation, and dynamic risk control into live trading, it is crucial to conduct rigorous and efficient backtesting using high-quality historical data to evaluate their robustness and feasibility. Leveraging its high-performance computing engine and powerful data processing capabilities, DolphinDB provides an ideal platform for medium- and high-frequency quantitative strategy backtesting. In this article, we demonstrate how to implement a full backtesting workflow using DolphinDB’s backtest plugin for a volatility-timed vertical spread strategy with option snapshot data.

An option is a financial contract that grants the buyer the right, but not the obligation, to buy or sell an underlying asset at a specified price on or before a given date. The price of an option is primarily influenced by several factors: the current price of the underlying asset (S0), the strike price (K), time to maturity (T), the expected future volatility of the underlying (σ), and the risk-free interest rate (r). Among these factors, future volatility (σ) is the only unobservable variable, making it the central component of option pricing and trading. In practice, pricing models such as the Black-Scholes-Merton (BSM) model are commonly used to infer implied volatility from market option prices, reflecting the market’s consensus expectation of future volatility.

In trading practice, volatility traders often construct delta-neutral portfolios to profit from mispricing or relative changes in implied volatility. For instance, when implied volatility is expected to rise, traders may establish positive vega positions such as long straddles. Conversely, when implied volatility is expected to decline, negative vega portfolios can be constructed to benefit from volatility compression.

Implied volatility can also serve as an important timing factor in directional option strategies. For example, if the market outlook on the underlying asset is moderately bullish and implied volatility is relatively low, traders may adopt a bull call spread. This allows them to gain directional exposure at a relatively low cost while limiting downside risk. Conversely, when the outlook turns moderately bearish and implied volatility is relatively high, a bear put spread can be employed to establish short exposure while keeping potential losses from upward price movements under control.

Building on this idea, we implement a vertical spread strategy that incorporates volatility timing signals . The strategy determines directional exposure based on the forecast of the underlying asset price and dynamically selects between a bull call spread and a bear put spread depending on the current implied volatility regime.

A typical medium- and high-frequency quantitative backtesting platform consists of three core components: market data replay, order matching simulation, and strategy execution with performance evaluation. However, implementing such systems presents several challenges:

-

Massive high-frequency datasets impose stringent requirements on query and computation performance.

-

The backtesting environment should closely simulate market conditions, including order execution probability, transaction prices, trading volume, and market impact.

-

The system architecture must be flexible and extensible to support diverse strategies and technical indicators.

To address these challenges, DolphinDB provides a high-performance and scalable backtesting framework based on its distributed storage and computing architecture. The solution consists of three critical components:

Market Data Replay

The replay feature streams historical data from one or more distributed tables into stream tables in strict chronological order or according to specified sorting rules. This provides a unified environment for both research and production, enabling real-time factor computation on historical data.

Matching Engine Simulator Plugin

The plugin supports both Level-2 tick-by-tick data and snapshot data. It follows the price-time priority matching rule and provides high-precision order execution simulation. Multiple matching modes and flexible parameter configurations are available to better emulate live trading environment.

Backtesting Framework

The backtesting framework allows users to define custom indicators and supports strategy evaluation based on tick-level, snapshot-level, minute-level, or daily data. It outputs comprehensive results including returns, positions, and detailed trade records. High-precision backtesting based on tick or snapshot data enables integrated validation of both simulation and historical backtests.

The solution’s modular structure allows for seamless integration with existing systems, accommodating users who may already deploy certain components in place. This adaptability enables traders to construct a comprehensive backtesting system from the ground up using DolphinDB's full suite of tools, or enhance their current setup by incorporating specific DolphinDB capabilities.

1. Option Volatility-Timing Spread Strategy Based on DolphinDB

1.1 Strategy Logic

In this article, we implement a volatility-timing options spread strategy on gold options using full intraday data from the Shanghai Futures Exchange (SHFE) and the DolphinDB Backtest plugin. The strategy logic is summarized below:

| Strategy Parameter | Value |

|---|---|

|

Start date |

2025-02-17 (Intraday start) |

|

End date |

2025-02-17 (Intraday end) |

|

Backtest frequency |

Snapshot-level |

|

Initial capital |

1,000,000 |

|

Underlying |

Call & Put options for the main gold futures contract |

|

Entry signals |

|

|

Position construction |

Positions are established in real time according to IV signals:

|

|

Exit signals |

The spread between the ATM and OTM option legs is monitored in real time for each option spread. For both bull call and bear put spreads, a widening ATM–OTM spread indicates increasing profit. Positions are closed with market orders when the relative change in the spread from its initial level reaches the predefined bounds of [-3%, 5%], where Relative change = (current spread − initial spread) / initial spread. |

1.2 Profit and Loss (P&L) Scenarios

We analyze the profit and loss of the option spreads used in the current strategy. Assume that the underlying gold futures price is 675 CNY/g. The corresponding ATM and two strikes OTM options for both the call and put directions, along with their opening premiums, are shown below.

| Option Type | Symbol | Premium Paid/Received to Open |

|---|---|---|

|

An ATM call option |

AU2503-C-672 |

C1 |

|

A call option two strikes OTM |

AU2503-C-688 |

C2 |

|

An ATM put option |

AU2503-P-672 |

C3 |

|

A put option two strikes OTM |

AU2503-P-656 |

C4 |

Note: Since the premium of an ATM option is higher than that of an OTM option, we have C1 > C2 and C3 > C4.

1.2.1 Bull Call Spread Option Position

Assume that IV is relatively low and the underlying futures price is trending upward, triggering a bull call spread signal—that is, buying an ATM call option and selling a call option two strikes OTM.

The underlying gold futures price (St) may evolve under the following three scenarios:

-

Significant decline (St << 672)

-

Moderate increase or sideways movement (672 ≤ St ≤ 688)

-

Significant increase (St >> 688)

For each of these scenarios, the P&L direction and magnitude of the ATM call, the call option two strikes OTM, and the overall option spread are summarized in the table below.

| Gold Futures | ATM Call Option (Long) | Call Option Two Strikes OTM (Short) | Bull Call Spread (1:1) |

|---|---|---|---|

|

Significant Decline |

|

|

|

|

Moderate Increase / Sideways |

|

|

The ATM option typically has a larger absolute delta than the OTM option, resulting in a net positive delta for the spread.

|

|

Significant Increase |

|

|

|

1.2.2 Bear Put Spread Option Position

Assume that IV is relatively high and the underlying futures price is trending downward, triggering a bear put spread signal—that is, buying an ATM put option and selling a put option two strikes OTM.

The underlying gold futures price (St) may evolve under the following three scenarios:

-

Significant decline (St<<656)

-

Moderate decrease or sideways movement (656≤St≤672)

-

Significant increase (St>>672)

For each of these scenarios, the P&L direction and magnitude of the ATM put, the put option two strikes OTM, and the overall option spread are summarized in the table below.

| Gold Futures | ATM Put Option (Long) | Put Option Two Strikes OTM (Short) | Bear Put Spread (1:1) |

|---|---|---|---|

|

Significant Decline |

|

|

|

|

Moderate Decrease / Sideways |

|

|

The ATM option typically has a larger absolute delta than the OTM option, resulting in a net negative delta for the spread.

|

|

Significant Increase |

|

Large Floating profit: the OTM put gains value rapidly as the underlying price rises.

|

|

1.2.3 P&L Summary

Both the bull call spread and bear put spread collect premium from selling options to offset the cost of buying the other leg. This strategy has two key characteristics:

-

Limited maximum loss: the total potential loss of the spread is capped at the initial net expenditure when the underlying moves in an adverse direction.

-

Limited maximum profit: the total profit is capped at the difference between strike prices minus the net premium paid.

By sacrificing unlimited upside potential, the strategy significantly lowers the breakeven point and reduces the required margin for hedging.

1.3 Strategy Structure

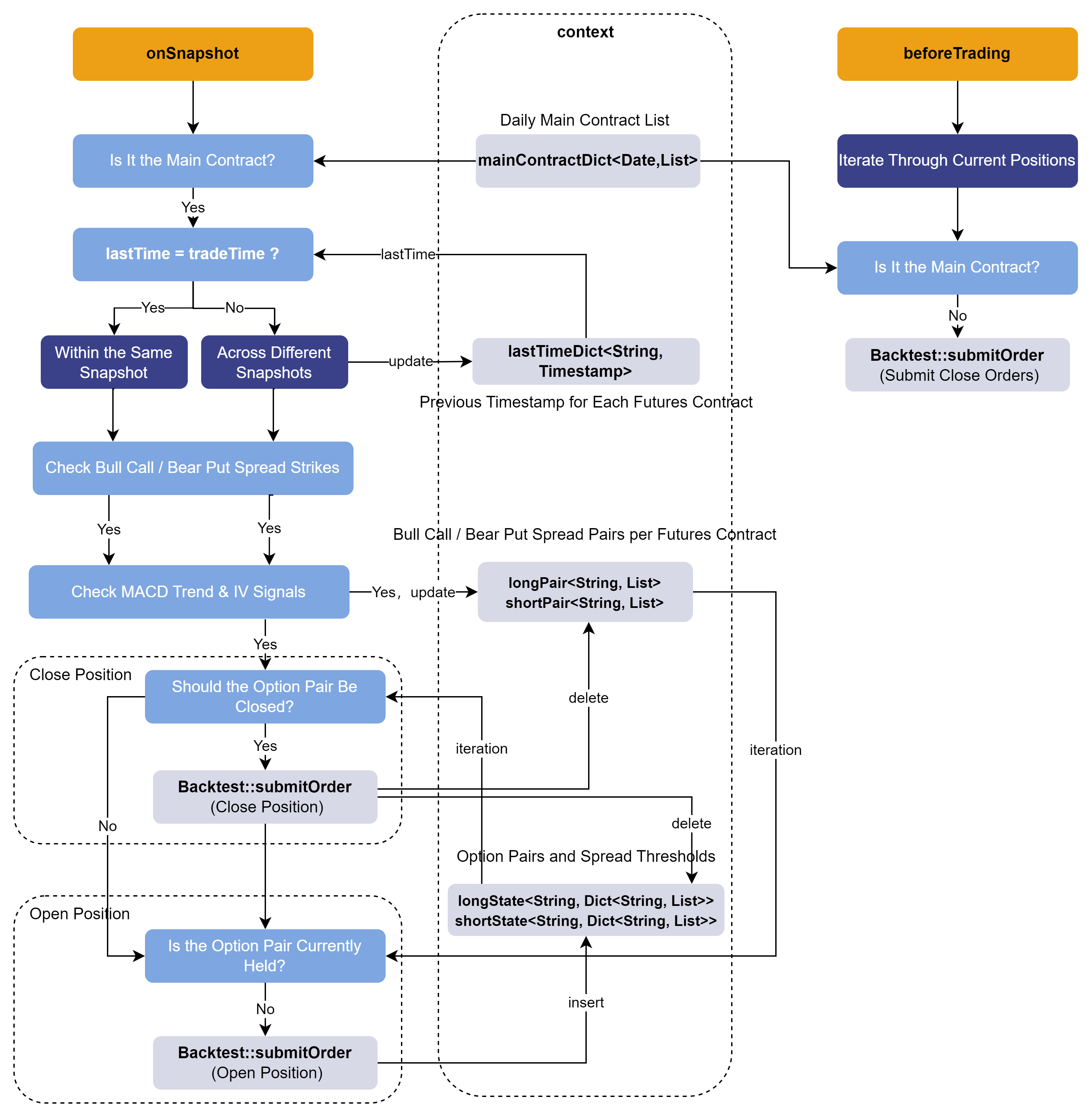

The DolphinDB Backtest plugin provides a variety of event-driven callback

functions, including onSnapshot , onBar , and

onTrade . The onSnapshot callback is

primarily used to implement the intraday option volatility-timing spread

strategy at snapshot frequency, in conjunction with the context state of the

DolphinDB Backtest plugin.

Within the context state, three types of variables are defined for the strategy:

-

lastTimeDict – stores the previous timestamp for each futures contract.

-

longPair and shortPair – represent the bull call spread and bear put spread option pairs for each futures contract, respectively.

-

longState and shortState – record the corresponding option pairs and the configured spread bounds for the bull call spread and bear put spread positions.

The overall implementation logic of the strategy is summarized as follows:

1.3.1 Retrieving Basic Information

Within the onSnapshot callback, three input parameters are

provided sequentially:

-

context: a dictionary to restore the context state.

-

msg: a dictionary to restore the snapshot market data.

-

indicator: the custom indicator object.

First, option contract information is collected, including the option symbol, the corresponding futures contract, option type (call/put), and strike price levels. Then, the list of the day’s main contract is obtained, and market data for non-main contracts is excluded.

def onSnapshot(mutable contextInfo, msg, indicator){

/* Snapshot callback

msg structure: a dictionary containing the data of an instrument in the snapshot

symbol->

symbolSource->

...

indicator: a dictionary containing the computed indicators of the instrument

...

*/

// Get instrument-level option information

ioption = msg.symbol // Option symbol

direction = contextInfo["directionDict"][ioption] // Call (1) or Put (2)

contract = contextInfo["contractDict"][ioption] // Underlying futures contract

strike = contextInfo["strikePriceDict"][ioption] // Option strike price

// Get the signal information

level = msg["signal"][0] // Option strike price levels

ivSignal = msg["signal"][1] // Options IV signal

trendSignal = msg["signal"][2] // Futures price MACD trend signal

// Get current time information

tradeTime = contextInfo["tradeTime"]

tradeDate = contextInfo["tradeDate"]

// Filter out non-main contracts

contractList = contextInfo["mainContractDict"][tradeDate] // Today's main contract list

if (!(contract in contractList)){ // Non-main contract

return

}

...

}1.3.2 Selecting Option Pairs

Since the latest price of the underlying futures changes in real time, it is

necessary to continuously track the strike price levels of the target

options. To support multi-symbol and multi-contract scalability in the

strategy, a nested dictionary with the structure <STRING,

Dict<STRING, VECTOR>> is used as a state variable. The

outer STRING indicates the futures contract symbol, the inner STRING

indicates the option pair name, and the VECTOR is a two-element string

vector corresponding to [ATM option symbol, two-strike OTM

symbol] . The two options within the vector form an option

pair, and the corresponding order logic is executed for each pair during the

subsequent position-opening process.

In the onSnapshot callback, the target option pairs are

selected in real time as follows:

-

All options are evaluated, and if an option is in the bull call spread direction (i.e., the ATM call and the call option two strikes OTM), it is placed into the longPair state variable; Otherwise, if it is in the bear put spread direction (i.e., the ATM put and the put option two strikes OTM), it is placed into the shortPair state variable.

-

During the subsequent opening logic, positions are established based on the option pairs stored in longPair and shortPair.

ivSignal = msg["signal"][1] // ivFactor

trendSignal = msg["signal"][2] // trendFactor

// Bull Call / Bear Put signals -> add to longPair & shortPair

if (ivSignal == 1 and trendSignal == 1){

// Bull Call signal triggered -> long ATM call + short call option two strikes OTM

if (!(contract in keys(contextInfo["longPair"]))){

contextInfo["longPair"][contract] = array(STRING, 2)

}

if (level == 0 and direction == 1){ // ATM call

contextInfo["longPair"][contract][0] = ioption

}else if (level == -2 and direction == 1){ // Call option two strikes OTM

contextInfo["longPair"][contract][1] = ioption

}

}else if (ivSignal == -1 and trendSignal == -1){

// Bear Put signal triggered -> long ATM put + short put two strikes OTM

if (!(contract in keys(contextInfo["shortPair"]))){

contextInfo["shortPair"][contract] = array(STRING, 2)

}

if (level == 0 and direction == 2){ // ATM put

contextInfo["shortPair"][contract][0] = ioption

}else if (level == -2 and direction == 2){ // Put two strikes OTM

contextInfo["shortPair"][contract][1] = ioption

}

}1.3.3 Constructing Cross-Sectional Order Execution

The onSnapshot callback is triggered once for each snapshot

of each instrument. Cross-sectional snapshots can be constructed by aligning

snapshots across instruments based on their timestamps, enabling the

implementation of cross-sectional order execution. Since the ingested data

is already sorted by timestamp, the tradeTime for each contract in the

callback is guaranteed to be monotonically increasing, so this logic is

valid.

The code for constructing cross-sectional snapshots within the

onSnapshot callback is as follows: for different

options within a single futures contract snapshot, the callback can

terminate immediately; only when the current timestamp differs from the

previous one—that is, when moving to the next cross-sectional snapshot for a

futures contract—should the corresponding state variables be retrieved from

the context to perform position closing and opening, after which the

remaining code logic continues to execute.

// Get current time information

... // Code block applied to all underlyings

tradeTime = contextInfo["tradeTime"]

if (contextInfo["lastTimeDict"][contract]==tradeTime){

return

}else{ // Next snapshot section

contextInfo["lastTimeDict"][contract]=tradeTime.copy()

}

... // Code block triggered only on snapshot change1.3.4 Closing Option Pair Positions

Based on the analysis in Section 2.1, the spread between the ATM and OTM options plays a crucial role in the final P&L of the option spreads constructed. Therefore, it is necessary to track the changes in the spread in real time and close the option pairs at the appropriate time.

The code segment for closing positions is shown below (taking the Bull Call Spread option pair as an example):

if (contract in keys(contextInfo["longState"])){

// longState stores [long ATM call, short call option two strikes OTM] -> Closing logic [Close Long, Close Short]

for (optPair in keys(contextInfo["longState"][contract])){

opt1 = optPair.split("$")[0] // ATM Call

opt2 = optPair.split("$")[1] // Call option two strikes OTM

price1 = contextInfo["lastPriceDict"][opt1]

price2 = contextInfo["lastPriceDict"][opt2]

state = price1 - price2 // Compute latest spread

stateList = contextInfo["longState"][contract][optPair] // Min & Max spread

// Check if spread breaks threshold

if (state<stateList[0] or state>stateList[1]){

vol1 = Backtest::getPosition(contextInfo["engine"], symbol=opt1)["longPosition"][0]

// ATM Call long

vol2 = Backtest::getPosition(contextInfo["engine"], symbol=opt2)["shortPosition"][0]

// OTM Call short

if (isNull(vol1) or isNull(vol2)){

continue

}

if (vol1>0 and vol2>0){

orderDirection = 3 // Close long

Backtest::submitOrder(contextInfo["engine"],

(opt1, "SHFE", tradeTime, 0, price1, price1, vol1, orderDirection, 0),

label="closeLong",orderType=0)

orderDirection = 4 // close short

Backtest::submitOrder(contextInfo["engine"],

(opt2, "SHFE", tradeTime, 0, price2, price2, vol2, orderDirection, 0),

label="closeShort",orderType=0)

// Remove spread record

contextInfo["longState"][contract].erase!(opt1+"$"+opt2)

contextInfo["longPair"] = array(STRING, 2)

}

}

}

}1.3.5 Opening Option Pair Positions

For the opening logic, the Backtest::getAvailableCash

function is used to check the real-time available cash, preventing orders

from being placed when funds are insufficient. Next, orders are executed

based on the bull call spread and bear put spread option pairs stored in

longPair and shortPair, respectively.

Note that to avoid duplicate orders, the

Backtest::getPosition function is used to retrieve the

current positions of the underlying and check whether there are existing

positions in the corresponding direction.

The code segment for opening positions is shown below (taking the bull call spread option pair as an example):

if (Backtest::getAvailableCash(contextInfo["engine"]) <= 100000){

return

}

// Bull call spread → long ATM call + short call option two strikes OTM

if (contract in keys(contextInfo["longPair"])){

opt1 = contextInfo["longPair"][contract][0]

opt2 = contextInfo["longPair"][contract][1]

vol1 = Backtest::getPosition(contextInfo["engine"], symbol=opt1)["longPosition"][0]

vol2 = Backtest::getPosition(contextInfo["engine"], symbol=opt2)["shortPosition"][0]

price1 = contextInfo["lastPriceDict"][opt1]

price2 = contextInfo["lastPriceDict"][opt2]

optPair = opt1+"$"+opt2

if (!isNull(opt1) and !isNull(opt2) and price1!=price2){ // Initial spread is not zero

// Check if current option is already held

state = false

if (!(isNull(vol1))){

if (vol1 >0){

state = true

}

}

if (!(isNull(vol2))){

if (vol2 >0){

state = true

}

}

if (!state){

// Open 1 lot

orderDirection = 1 // ATM Call long

Backtest::submitOrder(contextInfo["engine"],

(opt1, "SHFE", tradeTime, 0, price1, price1, 1, orderDirection, 0),

label="openLong",orderType=0) // Order (0: Market)

orderDirection = 2 // Short call option two strikes OTM

Backtest::submitOrder(contextInfo["engine"],

(opt2, "SHFE", tradeTime, 0, price2, price2, 1, orderDirection, 0),

label="openShort",orderType=0) // Order (0: Market)

// Add spread record

if (!(contract in keys(contextInfo["longState"]))){

contextInfo["longState"][contract] = dict(SYMBOL, ANY)

// Option pair code: [min spread, max spread]

}

contextInfo["longState"][contract][optPair] = [

(price1-price2) * (1-contextInfo["lowLimit"]),

(price1-price2) * (1+contextInfo["upLimit"])

]

}

}

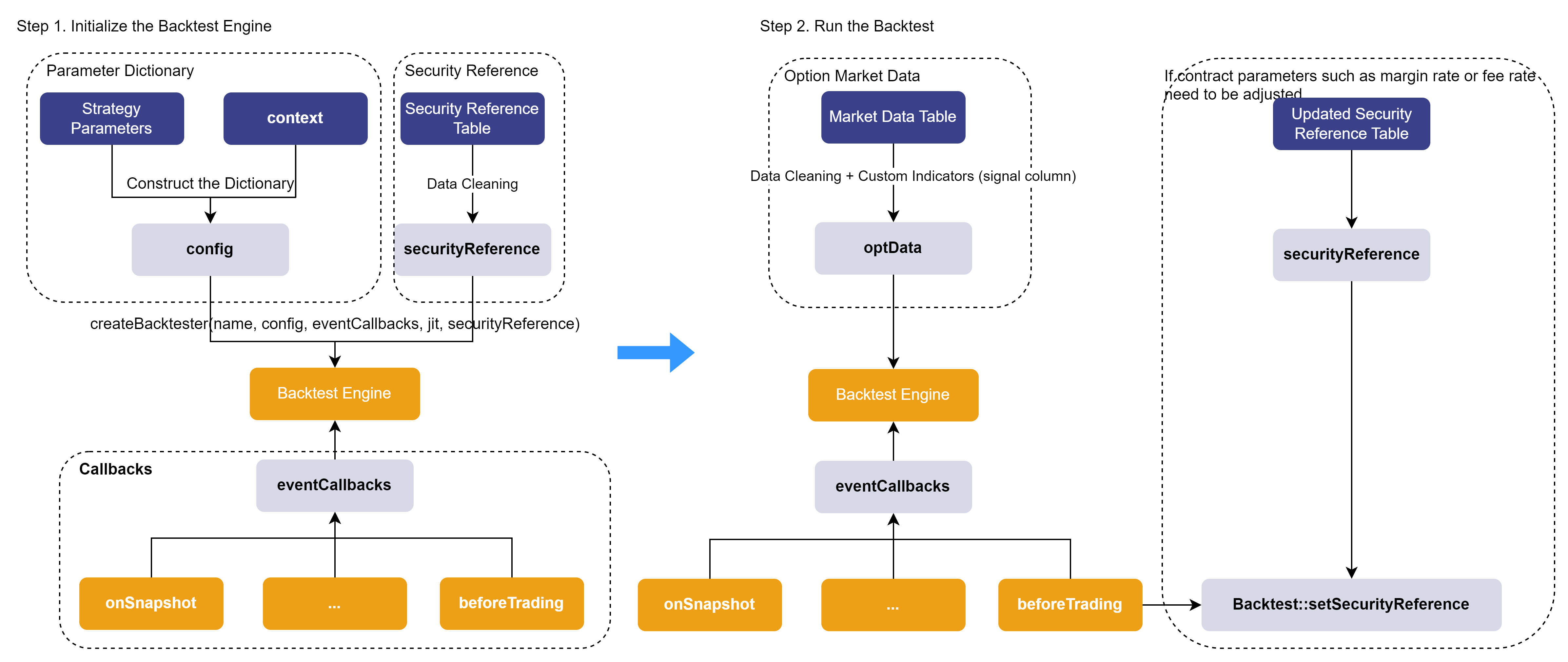

}2. Backtesting Workflow

This section demonstrates the full workflow for processing medium- and high-frequency option backtesting data using the Backtest plugin.

During backtesting, if parameters such as the contract’s multiplier, fee rate, or

margin change, these updates can be handled in the beforeTrading

pre-market callback. Then by calling Backtest::setSecurityReference

with the updated reference table, the backtesting can more accurately reflect real

trading conditions.

2.1 Creating the Backtesting Engine

The backtesting engine is created via the

Backtest::createBacktester function, which includes the

following key parameters:

-

eventCallbacks: a dictionary of callback functions used to define the strategy’s handling logic at different event triggers (e.g., market data updates, order matching results, etc.) (see the following paragraphs for details).

-

config: the engine configuration dictionary, containing various parameters required for strategy execution as well as the context dictionary for maintaining strategy state.

-

securityReference: the reference table of underlying contract information.

In this article, the cleaned option market data (optData) and the underlying

reference table (securityReference) are saved as CSV files and provided for

download in the attachments. You can load them using the

loadText function.

The complete code for creating the backtesting engine is as follows:

/* 1. Create Backtesting engine */

// Option reference table

filePath = "/ssd/ssd0/single16coreJIT/server/optionData/" // Replace with the CSV path on your DolphinDB server

schemaTb = table(["symbol","underlyingAssetType","multiplier","type","strikePrice","marginRatio","tradeUnit",

"priceUnit","priceTick","commission","deliveryCommissionMode","lastTradingDay","exerciseDate",

"exerciseSettlementDate","exDate","adjStrikePrice","adjMultiplier"] as `name,

["SYMBOL","INT","DOUBLE","INT","DOUBLE","DOUBLE","DOUBLE","DOUBLE","DOUBLE","DOUBLE","INT",

"DATE","DATE","DATE","DATE","DOUBLE","DOUBLE"] as `types)

securityReference = loadText(filePath+"optSecurityReference.csv",schema=schemaTb)

// Prepare Backtest configuration parameters

config = dict(STRING, ANY)

config["startDate"] = startDate // Backtest start date

config["endDate"] = endDate // Backtest end date

config["strategyGroup"] = "option" /// Strategy type

config["dataType"] = 1 // Use snapshot data

config["callbackForSnapshot"] = 0 // Effective when dataType==1, 0: trigger only onSnapshot, 1: trigger onSnapshot & onBar, 2: trigger only onBar

config["maintenanceMargin"] = 1.0 // Maintenance margin ratio

config["cash"] = 1000000

config["enableAlgoOrder"] = true // Enable algorithmic orders

config["outputOrderInfo"] = true // Output rejection reason

config["matchingMode"] = 3

config["latency"] = 50 // Simulated order latency (ms)

contractDict = dict(securityReference[`symbol], split(securityReference[`symbol],"-")[0])

directionDict = dict(securityReference[`symbol], securityReference[`type])

strikePriceDict = dict(securityReference[`symbol],securityReference[`strikePrice])

// Configure main contract information

mainContractDict = dict(DATE,ANY)

mainContractDict[2025.02.17] = ["AU2504"] // Store daily main contract list

// Configure context for Backtest

config["context"] = {

// Basic information

"lastTimeDict": dict(SYMBOL, TIMESTAMP), // {Futures symbol: last timestamp}

"contractDict": contractDict, // {Option symbol: Underlying futures contract}

"directionDict": directionDict, // 1 for Call, 2 for Put

"strikePriceDict": strikePriceDict, // {Option symbol: strike price}

"mainContractDict": mainContractDict, // {Date: main contract list}

// Signal settings

"upLimit": 0.05, // If option spread exceeds this percentage in profit direction, close both positions

"lowLimit": 0.03, // If option spread exceeds this percentage in loss direction, close both positions

"longState": dict(SYMBOL, ANY), // {Futures: {Bull Call pair: [min spread, max spread]}}

"shortState": dict(SYMBOL, ANY), // {Futures: {Bear Put pair: [min spread, max spread]}}

// Order-related

"lastPriceDict": dict(SYMBOL, DOUBLE), // Latest option price

"longPair": dict(SYMBOL, ANY), // Long option pair

"shortPair": dict(SYMBOL, ANY) // Short option pair

}

// Callback functions dictionary

eventCallBacks = dict(STRING, ANY)

eventCallBacks["initialize"] = initialize // Initialize function

eventCallBacks["beforeTrading"] = beforeTrading // Pre-trading callback

eventCallBacks["onSnapshot"] = onSnapshot // Snapshot callback

eventCallBacks["afterTrading"] = afterTrading // Post-trading callback

eventCallBacks["finalize"] = finalized // Finalize callback

try{Backtest::dropBacktestEngine(strategyName)}catch(ex){print(ex)} // Remove existing Backtesting engine

// Create backtesting engine

engine = Backtest::createBacktester(strategyName, config, eventCallBacks, jit, securityReference)

2.2 Executing the Backtest

This section describes how to compute the three core indicators used in the strategy—option strike level, MACD trend signal, and IV signal—which are stored in the signal column. It also explains how to pass market data containing these custom indicators into the backtesting engine to execute the backtest.

Step 1. Reading Market Data

Since this strategy only involves the main contracts, only the data of the main contracts is extracted.

// Load data and execute strategy backtest

schemaTb = table(["symbol","symbolSource","timestamp","tradingDay","lastPrice",

"upLimitPrice","downLimitPrice","totalBidQty","totalOfferQty",

"bidPrice","bidQty","offerPrice","offerQty","highPrice","lowPrice",

"prevClosePrice","prevSettlementPrice","underlyingPrice",

"Theta","Vega","Gamma","Delta","IV",

"contract","strike","direction"] as `name,

["SYMBOL","SYMBOL","TIMESTAMP","DATE","DOUBLE","DOUBLE","DOUBLE",

"LONG","LONG","DOUBLE[]","LONG[]","DOUBLE[]","LONG[]","DOUBLE",

"DOUBLE","DOUBLE","DOUBLE","DOUBLE","DOUBLE","DOUBLE","DOUBLE",

"DOUBLE","DOUBLE","SYMBOL","DOUBLE","INT"] as `types)

data = select * from loadText(filePath+"optData.csv",schema=schemaTb)

where symbol.startsWith("AU2504") // Only trade main contract

Step 2. Computing Option Strike Levels

Once the option market data has been retrieved, the strike levels are preprocessed using vectorized SQL operations for consistent use in the subsequent strategy logic. For both calls and puts, an INT-type strike level column is output: 0 indicates ATM options, -k indicates OTM options of level k, and k indicates ITM options of level k. The SQL code for computing option strike levels is as follows:

// Compute hourly spread

hourRank = select firstNot(strike)-firstNot(underlyingPrice) as priceDiff from data

group by contract, tradingDay, direction, symbol, hour(timestamp) as tradeHour

// Determine level rank within each hour

update hourRank set levelRank = iif(direction == 1,

rank(priceDiff,true), rank(priceDiff,false))

context by direction, contract, tradingDay, tradeHour

// Find ATM option within hourly cross-section (priceDiff closest to 0)

eqData = select sum(eqRank) as eqRank from (

select tradingDay, tradeHour, direction, contract,

iif(abs(priceDiff) == min(abs(priceDiff)), levelRank, 0) as eqRank from hourRank

context by tradingDay, tradeHour, direction, contract)

group by tradingDay, tradeHour, direction, contract

hourData = lj(hourRank, eqData, `tradingDay`tradeHour`direction`contract)

update hourData set levelRank = eqRank-levelRank

// Compute strikes price levels: 0=ATM, -k=OTM, +k=ITM

// Join back to original data

data = select * from data a left join (

select contract, tradingDay, direction, symbol, tradeHour, levelRank from hourData) b

on a.timestamp.hour() == b.tradeHour

and a.contract == b.contract

and a.tradingDay == b.tradingDay

and a.direction == b.direction

and a.symbol == b.symbol

order by timestamp ascStep 3. Generating Opening Signals

According to the strategy, a bull call spread opening signal is triggered when MACD turns from negative to positive and IV exceeds the 30-snapshot mean plus the standard deviation; a bear put spread opening signal is triggered when MACD turns from positive to negative and IV falls below the 30-snapshot mean minus the standard deviation. The code for computing MACD and IV signals is as follows:

/* Compute MACD trend signal */

macdFunc = def (lastPrice, short_=24, long_=52, m=18) {

dif = ewmMean(lastPrice, span=short_, adjust=false) -

ewmMean(lastPrice, span=long_, adjust=false)

dea = ewmMean(dif, span=m, adjust=false)

macd = (dif - dea) * 2

return round(macd, 4)

}

update data set macd = macdFunc(underlyingPrice).nullFill(0) context by symbol

update data set trendFactor = iif(macd>0 and prev(macd)<0, 1,

iif(macd<0 and prev(macd)>0, -1, 0)) context by symbol

/* Compute IV signal */

update data set ivLongLevel = mavg(IV.ffill(), 30) - mstd(IV.ffill(), 30) context by symbol

update data set ivShortLevel = mavg(IV.ffill(), 30) + mstd(IV.ffill(), 30) context by symbol

update data set ivFactor = iif(IV<ivLongLevel, 1.0, iif(IV>ivShortLevel, -1.0, 0.0)) // IV signalStep 4. Ingesting Data into the Engine

All custom indicators used during the backtest are merged into array vector via

the fixedLengthArrayVector function and passed into the

backtesting engine as part of the market data.

Finally, a data record with the symbol "END" is sent to the engine to indicate the backtest completion.

// Final data ingested into engine = market data + IV & Greeks + signals

data = select symbol, symbolSource, timestamp, tradingDay, lastPrice, upLimitPrice, downLimitPrice,

totalBidQty, totalOfferQty, bidPrice, bidQty, offerPrice, offerQty, highPrice, lowPrice,

prevClosePrice, prevSettlementPrice,

prevSettlementPrice as settlementPrice,

underlyingPrice, Theta, Vega, Gamma, Delta, IV,

fixedLengthArrayVector(double(levelRank),double(ivFactor),double(trendFactor)) as signal

from data

order by timestamp asc

timer Backtest::appendQuotationMsg(engine, data) // ingest snapshot data into backtesting engine

// Set END signal

endSignal = select * from data where timestamp = max(timestamp) limit 1

update endSignal set symbol = "END"

Backtest::appendQuotationMsg(engine, endSignal)

go3. Strategy Evaluation

3.1 Strategy Results

After the overall strategy has been executed, the following functions can be used to view the backtesting results.

// View backtesting results

contextInfo = Backtest::getContextDict(engine) // Final context dictionary

tradeDetails = Backtest::getTradeDetails(engine) // Trade details table

openOrders = Backtest::getOpenOrders(engine) // Open orders at the end of day

totalPosition = Backtest::getPosition(engine) // Current positions

dailyPosition = Backtest::getDailyPosition(engine) // Daily position table

enableCash = Backtest::getAvailableCash(engine) // Final available cash

dailyPortfolios = Backtest::getDailyTotalPortfolios(engine) // Daily P&L metrics table

returnSummary = Backtest::getReturnSummary(engine) // Summary analytics tableHere we show the results from tradeDetails (executed orders). The figure shows that the strategy results are consistent with the trading logic:

-

After a bull call spread signal was triggered, at 09:30:25, the option pair AU2504-P-672 & AU2504-P-656 was executed, with a spread of 11.58 - 5.68 = 5.9.

-

At 09:51:06, the spread of the same option pair dropped to 11.1 - 5.4 = 5.7, reaching the lower bound of the spread change threshold, so the option pair was closed at market.

3.2 Strategy Performance

The DolphinDB Backtest plugin supports JIT optimization to improve backtesting

performance. When creating the backtesting engine via

Backtest::createBacktester , setting the jit

parameter to true enables JIT optimization. This article compares backtesting

performance with and without JIT optimization using identical parameters and

data. The test results are as follows:

| Ingested Records | Executed Order Count | Backtest Time | Processing Rate (records/s) | |

|---|---|---|---|---|

|

Without JIT |

283,177 |

38 |

2.39 s |

118,484 |

|

With JIT |

283,177 |

38 |

1.51 s |

187,534 |

Regardless of JIT, the Backtest plugin achieves a market data processing rate exceeding 100,000 records/s. Enabling JIT improves performance by over 50% compared to running without JIT.

JIT Considerations:

-

The DolphinDB Backtest plugin supports JIT optimization only on DolphinDB Server version 3.00.2 or above.

-

When enabling JIT in the Backtest plugin, in some cases the input data structure may need to be adjusted.

-

When JIT optimization is enabled, tables cannot be accessed directly in callback functions. To process the data, they need to be converted into dictionaries.

3.3 Test Environment Configuration

DolphinDB server was installed and configured in cluster mode. The hardware and software environments for this test are as follows:

Hardware Environment

| Component | Specification |

|---|---|

|

Kernel |

3.10.0-1160.88.1.el7.x86_64 |

|

CPU |

Intel(R) Xeon(R) Gold 5220R CPU @ 2.20GHz |

|

Memory |

512 GB |

Software Environment

| Component | Version / Configuration |

|---|---|

|

Operating System |

CentOS Linux 7 (Core) |

|

DolphinDB Server |

3.00.4 2025.09.09 LINUX_JIT x86_64 |

|

DolphinDB License Limit |

16 cores, 128 GB |

4. Conclusion

This article demonstrates the implementation of a snapshot-frequency option spread strategy with integrated volatility timing using the DolphinDB Backtest plugin. It also outlines the full workflow for medium- and high-frequency option strategy backtesting and provides SQL scripts for computing option strike levels and trading signals.

The core logic of the strategy is to establish directional positions at a relatively low cost using bull call spread and bear put spread option pairs based on the current underlying futures price trend and option implied volatility level, while continuously monitoring the spread of each option pair to implement profit-taking and stop-loss closures in real time.

This case highlights the Backtest plugin’s excellent performance, rich strategy trigger mechanisms, and comprehensive backtesting evaluation results, offering practical reference for medium- and high-frequency trading strategy backtesting in the FICC domain.

5. FAQ

Handling Contract Rollover in Long-Term Backtests

In long-term option backtests, the strategy needs to handle contract rollover logic. The approach differs slightly for financial and commodity options:

-

For financial options: the front-month contract is treated as the main contract. To track it, an in-memory table can be maintained in the context state dictionary, storing product, contract, and remaining time to expiration. The strategy determines the current main contract based on remaining days to expiration. On rollover days, both the expiring contract and the new main contract data should be ingested into the backtesting engine to allow for closing positions of the expiring contract. On non-rollover days, only the current main contract needs to be ingested.

-

For commodity options: the daily main contract can be identified using futures snapshot data to compute contract OHLC bars and continuous futures contracts, or by referencing an existing table of main contracts. Once identified, the corresponding contract data is ingested into the backtesting engine, with rollover handling logic following the same pattern as for financial options.

Appendix

-

Backtesting script: backtesting.dos

-

Data: data.zip